E*TRADE Rollover IRA

Take control of your 401(k)

When you roll over a former employer's 401(k) or 403(b) to an E*TRADE IRA, you may enjoy a wider range of investment choices, lower costs, and greater control—all while preserving important tax advantages.

Get up to $10,000 for a limited time1

Why choose E*TRADE for my rollover?

Get control, choice, and support when you need it.

Fewer accounts to track

Put your retirement accounts under one roof, with one login so you can see the full picture.

Control your investing

DIY trading, long-term investing, or a mix—your IRA doesn’t have to be limited to employer plans.

Low costs, clear pricing

$0 commissions for most online trades, plus no annual IRA account fees and no minimums.2

Support when you need it

Speak with a Retirement Specialist who can help guide your rollover from start to finish and beyond.

Did you know?

Each year, about 2.8 million 401(k) accounts are left behind after job changes, potentially missing out on significant long-term savings if left untended.3

How to get started

Have questions or need assistance? Call 877-921-2434 to speak with a Retirement Specialist.

How to get started

Have questions or need assistance? Call 877-921-2434 to speak with a Retirement Specialist.

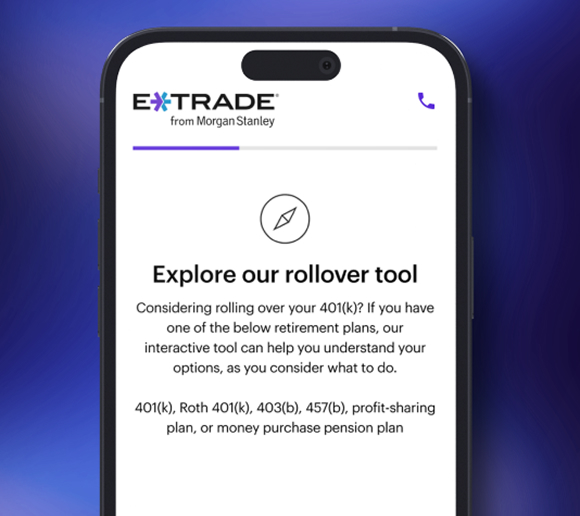

E*TRADE Rollover IRA tool

Is a rollover a good fit for you?

Answer a few simple questions in our E*TRADE Rollover IRA tool for insights to help you evaluate your next steps.

Four things you should consider before rolling over your 401(k)

Before you roll over a 401(k), take a minute to compare your options: leave it where it is, move it to a new employer plan, cash out, or roll it into an IRA.

Low fees, wide range of investments

Explore hands-off and low-cost options

Target date funds

Pick a fund whose target date is similar to the date you intend to retire. These ETFs are designed to help reduce your exposure to riskier investments as your retirement date approaches.

E*TRADE No Fee Index Funds

Get broad market exposure with E*TRADE’s lineup of no-fee index mutual funds—built to track key parts of the market with no fund expense ratio on these specific offerings.7 Other fees may apply.2

Get up to $10,000 cash credit1

Awards and recognition

E*TRADE Rollover IRA recognized in Stockbrokers.com “Best Rollover IRA accounts for 2026” review, winning “Best rollover IRA withdrawal options.”

Stockbrokers.com 2026 Review8

Explore similar accounts

Automated investment management

Core Portfolios9

For tax-free growth potential and withdrawals

Roth IRA10

Advice that meets you where you are

Managed Portolios

Education and resources

Insights to stay informed and inspired

Understanding IRA rollovers

Learn the key differences between direct and indirect rollovers—including timing, withholding, and rules that can trigger taxes and penalties.

What are target date funds 101?

Target date funds try to take the complexity out of retirement investing and reduce your exposure to riskier investments as you near retirement age.

A simple six-step retirement savings checkup

When market volatility arises, checking in on your retirement plan may make more than just sense.

Five ways to help your retirement savings last

If your retirement lasts longer than you expect, will you be ready? Here’s how to make your money last.

Frequently asked questions

-

- Must be 18 years of age or older

- To apply online, must be a US citizen or resident

- Generally, an investor cannot roll over assets from an employer's plan into an IRA unless they have changed jobs, retired, or are over age 59½

- An investor may also roll over into a Roth IRA if they have made after-tax contributions to a Roth 401(k) or Roth 403(b), or want to convert a pre-tax 401(k) to a Roth IRA

-

Whether you changed jobs or retired, you have options about what to do with your old 401(k), 403(b), or other former employer plan.

- You can leave assets in a former employer's plan.

- You can consolidate former plan assets to a current employer's retirement plan.

- You can consolidate former plan assets into an IRA.

- You can cash out.

-

A rollover generally takes 4–6 weeks to complete. However, this timeframe depends on how long the former employer or plan administrator takes to process the transaction.

-

A Traditional, Rollover, or Roth IRA account must first be opened with E*TRADE, unless account assets will be rolled over into an existing IRA.

Contact the benefits administrator of the former employer and complete all distribution forms required to initiate the direct rollover.

For rollovers via check:

Instruct the plan administrator to issue a distribution check made payable to:

Morgan Stanley, FBO

If rolling over to a Rollover IRA:

Make sure the Rollover IRA account number is included on the check.

If rolling over to a Roth IRA:

Make sure the Roth IRA account number is included on the check.

If rolling over to a Rollover and Roth IRA, separate checks must be issued for each.

Instruct the plan administrator to mail the check to:

E*TRADE from Morgan Stanley

PO Box 484

Jersey City, NJ 07303-0484

If the plan administrator sends you the check, simply forward it along with an IRA Deposit Slip to E*TRADE at the address above.

For securities rollovers:

Instruct the plan administrator to forward securities to DTC Clearing 0015, Code 40.

Or, if the plan administrator wants to mail certificates, make sure the certificates clearly indicate the E*TRADE Rollover or Roth IRA account number and are registered to the following:

Morgan Stanley, FBO

Instruct the plan administrator to mail the certificates to:

E*TRADE from Morgan Stanley

PO Box 484

Jersey City, NJ 07303-0484

-

Yes. Any amounts rolled over directly from a pre-tax employer plan into a Traditional or Rollover IRA are reportable, but not taxable. The former employer will send IRS Form 1099-R, which reports the plan distribution. E*TRADE will then send IRS Form 5498 by May 31 of the following year, reporting the incoming rollover to offset the distribution. However, if a pre-tax qualified plan is rolled over into a Roth IRA, this transaction is taxable and must be included in taxable income. Consult with a tax advisor for more information.

-

Generally, assets from an employer’s plan cannot be rolled over unless the participant has changed jobs, retired, or is over age 59½. Check with the employer's plan administrator to confirm whether assets may be transferred while still employed.

-

Rollovers and transfers are two different ways of moving funds:

- A direct rollover is the movement of assets from an employer's qualified retirement plan, such as a 401(k) to an IRA. Assets are sent directly from the plan administrator to the IRA custodian. A direct rollover is reportable on tax returns, but not taxable.

- A transfer is the movement of IRA assets held by one trustee or custodian to an identically registered IRA held by another trustee or custodian, without taking physical receipt of the funds. Account transfers are not reportable on tax returns and can be completed an unlimited number of times per year.