The basics of bond ladders

E*TRADE from Morgan Stanley

06/30/25Summary: Discover how you can build a bond ladder to generate predictable returns while helping diversify your portfolio and manage risk.

Building a bond ladder can be a smart way to help diversify your fixed income portfolio and manage risk. By purchasing bonds with staggered maturities, you can create a steady stream of predictable returns and potentially increase your average yield over time, while helping to mitigate interest rate and credit risks. Understanding how to construct a bond ladder is crucial if you want to maximize its potential benefits.

Let’s explore how it works.

How to build a bond ladder

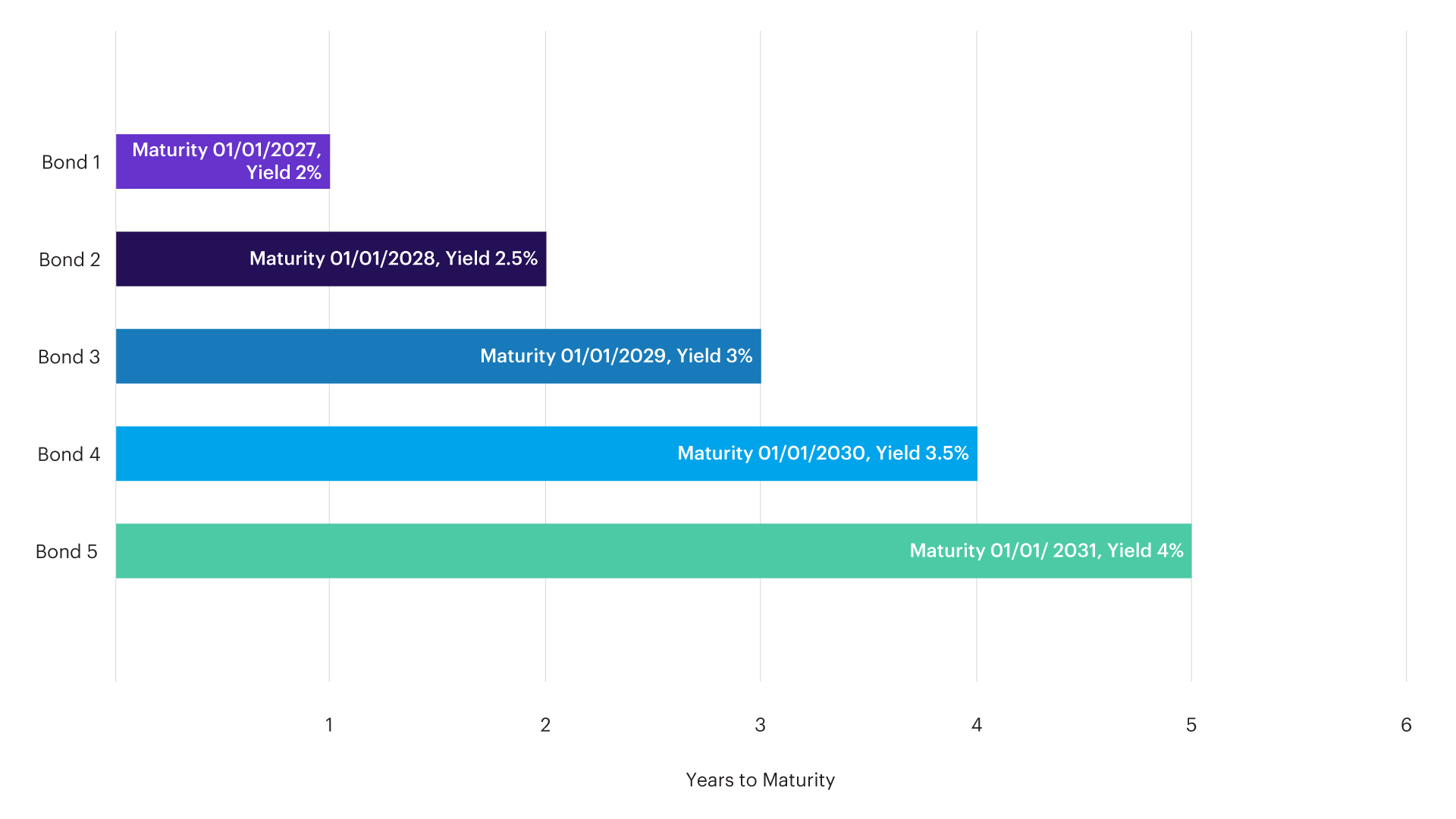

Suppose on January 1, 2026, you purchase five bonds with the following maturity dates. Under this structure, you will have one bond from your ladder maturing annually. With equal weighting and pricing across each rung, this ladder would have a combined average annual yield of 3.00%.

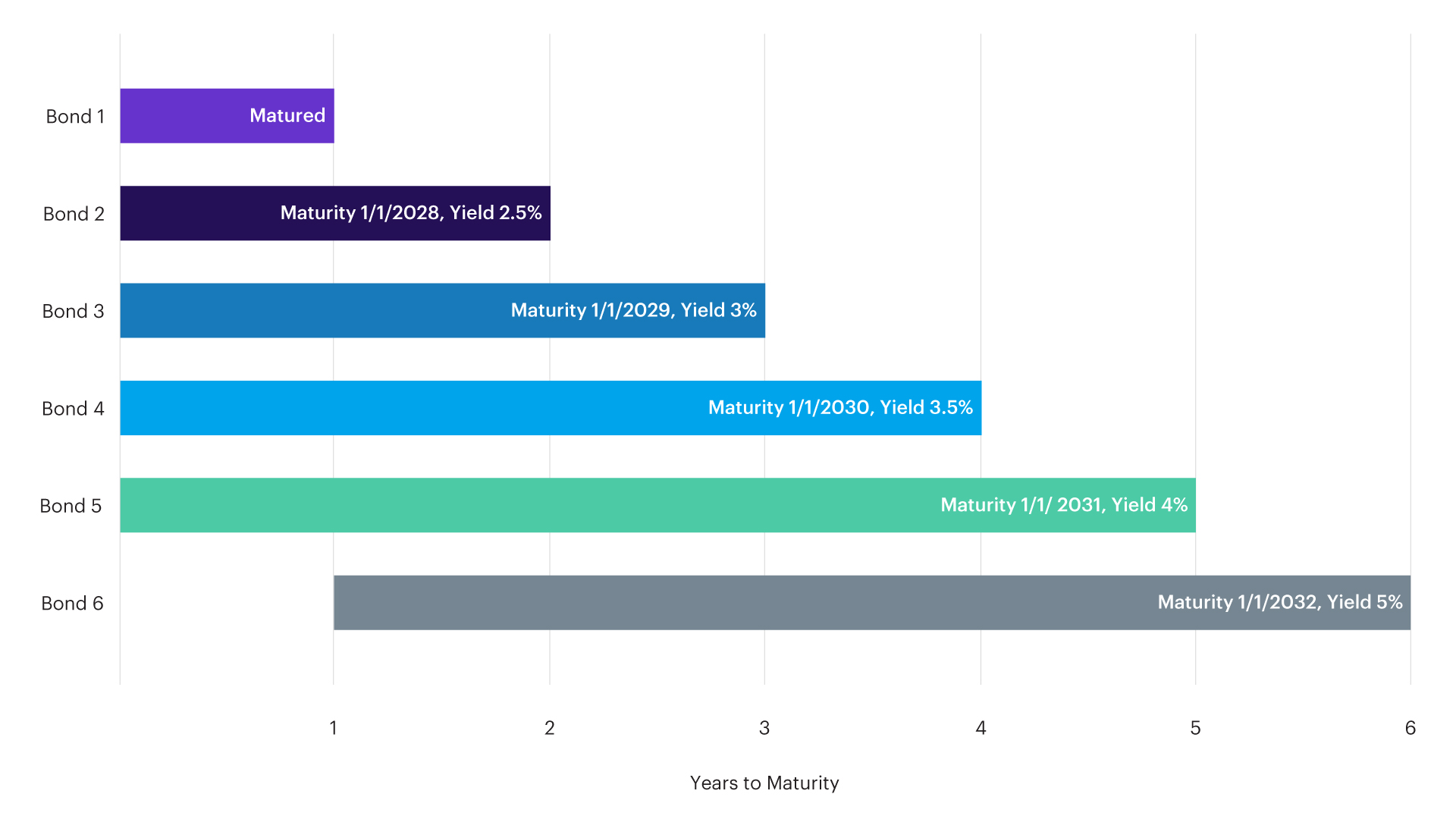

One year later, on January 1, 2027, you will receive a lump sum principal payment for the first maturing bond. In order to maintain a five-year ladder, you need to use the proceeds to buy a new bond maturing in five years.

By replacing the matured bond with a new bond maturing in five years, the structure of the ladder remains intact and you can continue to expect an annual principal payment. Eventually, the ladder will contain only bonds with five year terms to maturity. Since longer-term bonds tend to offer higher yields than shorter-term ones, this is likely to increase your average yield while maintaining the average maturity.

Why use a bond ladder?

Predictable returns

One of the most important benefits of a bond ladder is that it delivers predictable returns (assuming no defaults occur). Because bonds pay interest and principal according to a predetermined schedule, you can calculate exactly how much money you can expect to receive during the life of the ladder.

Suppose all of the above bonds pay coupons on January 1 and July 1. You can easily calculate your income on those two dates by adding up all of your expected cash flows from each bond. Likewise, you know exactly how much money you should receive in principal payments each time a bond matures.

This predictability is quite different from the behavior of a bond fund, which is inherently uncertain. The dividend payments float as the bonds in the fund change, and the value of the share price changes daily.

Risk management

Another key benefit of bond ladders is that they are a great way to manage two major risks facing fixed income investors.

1. Interest rate risk

When you buy a typical individual bond and hold it to maturity, the coupon payment you receive remains unchanged during the life of the bond. Locking in these fixed interest payments can be appealing when market rates are stable or falling, but it can be problematic when market rates are increasing above the rate on the bonds you own.

With a bond ladder, you can control the amount of exposure you have to changing rates:

- If you think rates are likely to rise, you can create a short-term ladder with frequent maturity dates to reinvest the proceeds at higher rates as the bonds mature.

- Conversely, if you think rates are near a peak, you can build a long-term ladder with infrequent maturity dates to lock in the current higher rates for a longer period.

- If you don’t have a strong opinion, you can compromise by creating a medium-term ladder.

The above example demonstrates how a short-term ladder with annual maturities allows you to take advantage of expected rate increases. Since a rung of this hypothetical ladder will mature each year for the next five years, you will receive principal to reinvest annually. As rates begin to increase, you will be in an excellent position to purchase new bonds with higher coupons (and longer maturities, depending on your investment horizon). If rates stay low, you can simply purchase another five-year bond and wait until next year.

2. Credit risk

Buying individual bonds exposes investors to credit risk, the possibility that a bond issuer will default on their debt (i.e., that they won’t pay back the lender).

Bond ladders help reduce the impact of defaults because they increase your portfolio's diversification. Rather than buying a single bond with 100% of your capital, a ladder distributes your investment across multiple bonds (as shown above), thereby helping limit your exposure to the risks of any single bond issuer defaulting.

By purchasing bonds with staggered maturities, you can create a steady stream of predictable returns and potentially increase your average yield over time, while helping to mitigate interest rate and credit risks.

An example:

On January 1, 2026, you have $5,000 to invest, and you want to keep the average maturity of your investment to no more than three years.

One option could be to buy five bonds, each maturing in three years. If the yield for these bonds at that time is 3%, then you would expect to receive interest payments totaling $450 over three years and a lump sum principal payment of $5,000 at the end of three years:

Option 1: Invest $5,000 in one bond with a 3-year term

| Expected interest income | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Purchase date | Maturity date | Yield | Investment | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Total | |

| 3-year bond | 1/1/2026 | 1/1/2029 | 3.0% | $5,000 | $150 | $150 | $150 | – | – | $450 |

*Hypothetical examples are for illustrative purposes only and are not intended to represent future performance of any particular award or investment. Your actual results may differ. The principal value and investment return of an investment will fluctuate with changes in market conditions, which may be worth more or less than original cost. Taxes may be due upon sale or exercise.

An alternative might be to build a bond ladder with an average maturity of three years by purchasing five bonds, staggering maturities of each by one year so that the first bond matures on January 1, 2027, and the last on January 1, 2031. If the yield for each bond is half a percentage point higher for each additional year of maturity, then you would expect to receive interest payments totaling $500 over five years and a lump sum principal payment of $1,000 at the end of each year:

Option 2: Invest $5,000 in bond ladder with an average maturity of three years

| Expected interest income | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Purchase date | Maturity date | Yield | Investment | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Total | |

| 1-year bond | 1/1/20246 | 1/1/2027 | 2.0% | $1,000 | $20 | – | – | – | – | $20 |

| 2-year bond | 1/1/2026 | 1/1/2028 | 2.5% | $1,000 | $25 | $25 | – | – | – | $50 |

| 3-year bond | 1/1/2026 | 1/1/2029 | 3.0% | $1,000 | $30 | $30 | $30 | – | – | $90 |

| 4-year bond | 1/1/2026 | 1/1/2030 | 3.5% | $1,000 | $35 | $35 | $35 | $35 | – | $140 |

| 5-year bond | 1/1/2026 | 1/1/2031 | 4.0% | $1,000 | $40 | $40 | $40 | $40 | $40 | $200 |

| Total | $150 | $130 | $105 | $75 | $40 | $500 | ||||

*Hypothetical examples are for illustrative purposes only and are not intended to represent future performance of any particular award or investment. Your actual results may differ. The principal value and investment return of an investment will fluctuate with changes in market conditions, which may be worth more or less than original cost. Taxes may be due upon sale or exercise.

Option 3: Invest $5,000 in a 5-rung bond ladder with an average maturity of three years and reinvest the proceeds every year for another five years

| Expected interest income | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Purchase date | Maturity date | Yield | Investment | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Total | |

| 1-year term | 1/1/2026 | 1/1/2027 | 2.0% | $1,000 | $20 | – | – | – | – | $20 |

| 2-year term | 1/1/2026 | 1/1/2028 | 2.5% | $1,000 | $25 | $25 | – | – | – | $50 |

| 3-year term | 1/1/2026 | 1/1/2029 | 3.0% | $1,000 | $30 | $30 | $30 | – | – | $90 |

| 4-year term | 1/1/2026 | 1/1/2030 | 3.5% | $1,000 | $35 | $35 | $35 | $35 | – | $140 |

| 5-year term | 1/1/2026 | 1/1/2031 | 4.0% | $1,000 | $40 | $40 | $40 | $40 | $40 | $200 |

| 5-year term | 1/1/2027 | 1/1/2032 | 4.0% | $1,000 | – | $40 | $40 | $40 | $40 | $160 |

| 5-year term | 1/1/2028 | 1/1/2033 | 4.0% | $1,000 | – | – | $40 | $40 | $40 | $120 |

| 5-year term | 1/1/2029 | 1/1/2034 | 4.0% | $1,000 | – | – | – | $40 | $40 | $80 |

| 5-year term | 1/1/2030 | 1/1/2035 | 4.0% | $1,000 | – | – | – | – | $40 | $40 |

| Total | $150 | $170 | $185 | $195 | $200 | $900 | ||||

*Hypothetical examples are for illustrative purposes only and are not intended to represent future performance of any particular award or investment. Your actual results may differ. The principal value and investment return of an investment will fluctuate with changes in market conditions, which may be worth more or less than original cost. Taxes may be due upon sale or exercise.

As illustrated above, bond ladders work best when the yield on the bonds to be bought in the future years is higher than the current yield. Visit our Bond Ladder Builder for step-by-step guidance on constructing a ladder tailored to your unique investing objectives.

CRC# 4610851 06/2025

How can E*TRADE from Morgan Stanley help?

Need help getting started with bonds?

To get started with bonds, visit our comprehensive Bond Resource Center. Use our Advanced Screener to quickly find the right bonds for you. Or call our Fixed Income Specialists at (877-355-3237) if you need additional help.

Brokerage account

Investing and trading account

Buy and sell stocks, ETFs, mutual funds, options, bonds, and more.

Bonds and CDs

These investments pay regular interest and typically aim to return 100% of their face value at maturity. Choices include everything from U.S. Treasury, corporate, and municipal bonds to FDIC-insured certificates of deposit (CDs).

Individual bonds and CDs

Explore over 50,000 bonds from 200+ leading providers. Most bonds and certificates of deposits (CDs) are designed to pay you steady income on a regular basis.