IRAs for Minors: How an early start can help boost retirement savings

E*TRADE from Morgan Stanley

03/17/23Have you ever crunched your numbers through an online retirement savings calculator and thought, “If only I had 10 more years? Just think of where my nest egg could be now!”

While you can’t turn the clock back and start over, you can help your children. When it comes to investing, it can sometimes feel like the early bird gets the biggest worm.

But just how early can your children start investing in their own retirement? According to the IRS, they can start as soon as they start earning income.

What kind of income? Earnings from a summer job or even mowing a neighbor’s lawn can qualify. If you own a sole proprietorship or LLC, you may be allowed to hire your child as a part-time employee and deduct their wages as a business expense. (E*TRADE from Morgan Stanley is not a tax advisor nor do we provide tax advice so be sure to talk to your tax professional first.)

How much of a difference can early investing make?

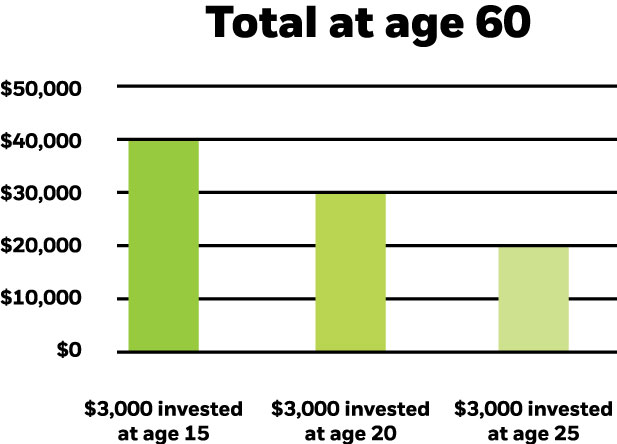

Even a modest contribution can add up over time thanks to the power of compound growth. Consider this: $3,000 invested today would be worth about $40,000 in 45 years, assuming a hypothetical 6% annual return, compounded monthly. That’s not a bad start to a retirement nest egg.

Time is on your side when it comes to compounding growth. For example: If the investor mentioned above waited just five more years before investing the $3,000, the savings may be worth about $12,000 less. Wait ten years, and the total could potentially drop by almost $20,000.

Hypothetical values are approximations. The example presented is hypothetical in nature and not intended to predict, project, or guarantee the performance of an actual investment or strategy. Charges, expenses, and taxes, which could be associated with an actual investment or strategy and which would lower returns, are not reflected. Individual investor results will vary.

Even if your children don’t have their eyes set on future savings, you can still help by offering to match any earned funds, with the caveat that these earnings are invested in an IRA. The benefits of this strategy are two-fold: Your children may benefit from potential compound growth during those critical, early years, and at the same time, get a first-hand look at how investing early and often may benefit their financial future. That’s definitely a lesson worth learning.

How does an IRA for minors work?

A child under 18 years old with earned income can contribute as much as they earn during the year, up to the maximum annual limit. A babysitter who earns $2,500 during the year can contribute $2,500 into an IRA, for example. They should be sure to keep a written log of their earnings, especially if they won’t be filing their own tax return or receive a W-2 from an employer.

Then there are the tax advantages, particularly for the Roth IRA, which allows earnings to potentially grow tax-free. Remember that $3,000 investment that grew to about $40,000 over 45 years? A Roth account owner won’t owe any federal taxes (and possibly state taxes, depending on their state of residence) on future distributions if certain conditions are met. That can be huge.

Additionally, Roth IRA contributions are typically made with post-tax dollars. Many teen workers aren’t likely to earn more than their annual standard deduction, which means they won’t owe any income taxes on their Roth IRA contribution either.

While withdrawing from an IRA should be a last resort, contributions can generally be taken out of a Roth IRA pretty much any time, without a tax hit. Earnings are a different story. Unless the distribution satifies the qualified distribution of earnings will be subject to ordinary income tax and, if made before age 59 ½, a 10% penalty tax (unless an exception applies).

If you want to help your children start saving early, consider opening an IRA for Minors. These accounts give you control over the assets until your child reaches the age of majority (or legal contract age) in the state in which you live.

Let E*TRADE from Morgan Stanley help

If you have any questions about an IRA for Minors or need help getting started, give us a call at 877-921-2434.