Market confronts new normal

E*TRADE from Morgan Stanley

As expected, the Federal Reserve held interest rates steady at its latest policy meeting, leaving the benchmark fed funds rate in its 5.25%-5.5% target range. The question is how investors will continue to adjust to what is likely to be the “new normal”—a higher-for-longer rate environment, regardless of whether the Fed hikes again at a later date.

With the US stock market losing ground again in October and bonds continuing to sell off, some investors may be feeling challenged in a way they haven’t since 2022. And last month’s geopolitical turmoil, Capitol Hill distractions, and energy market volatility didn’t do anything to improve market sentiment.

These are the times when discipline and diversification really matter.

The good news: Interest rates have simply moved closer to their long-term historical norms after an extended period of being abnormally low. And while a high-rate environment may not be as forgiving as the previous “free money” era—it will force investors (and businesses) to be more judicious about their choices—disciplined investors who maintain exposure to different segments of the market can keep themselves on track for long-term success.

In short, this is the type of environment where discipline, diversification, and rebalancing really matter.

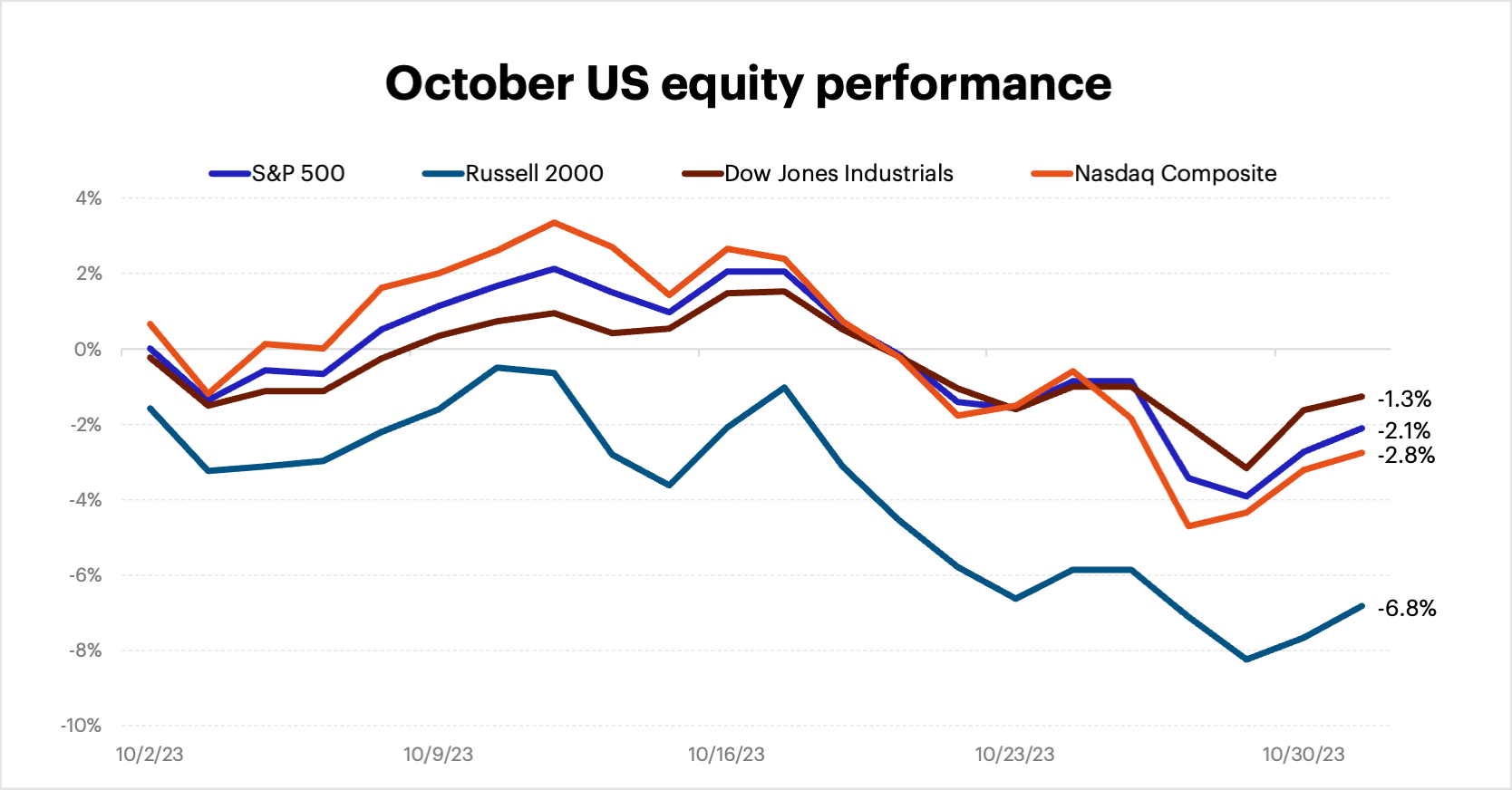

US equities

The S&P 500 declined for a third-straight month in October, falling 2.1%. The tech-heavy Nasdaq Composite fell slightly more (-2.8%), while the small-cap Russell 2000 lost the most ground (-6.8%):

FactSet Research Systems. (It is not possible to invest in an index.)

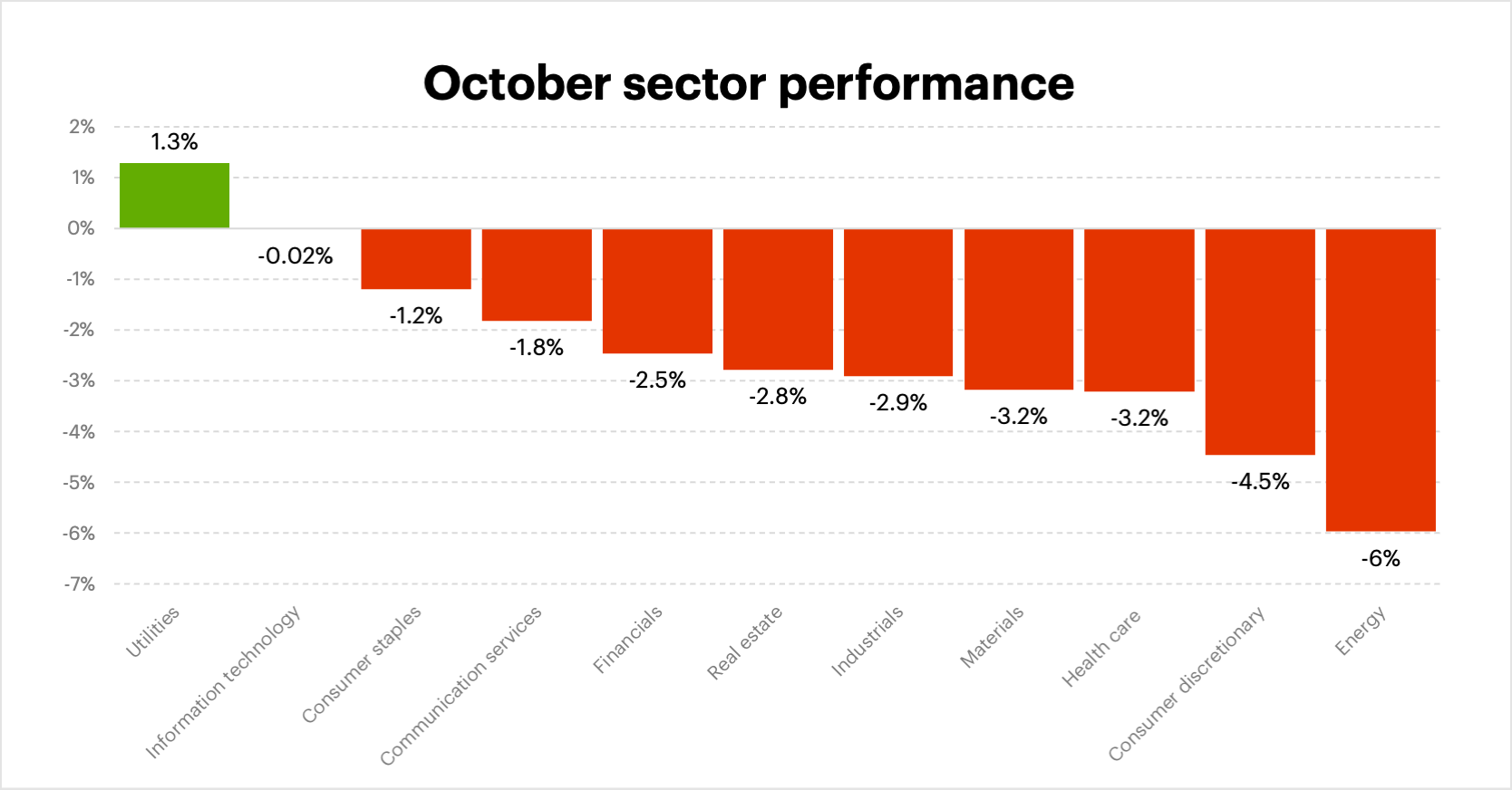

Sectors

While utilities appeared to benefit from defensive buying last month, all other S&P 500 sectors were negative, with energy and consumer discretionary stocks falling the most:

FactSet Research Systems

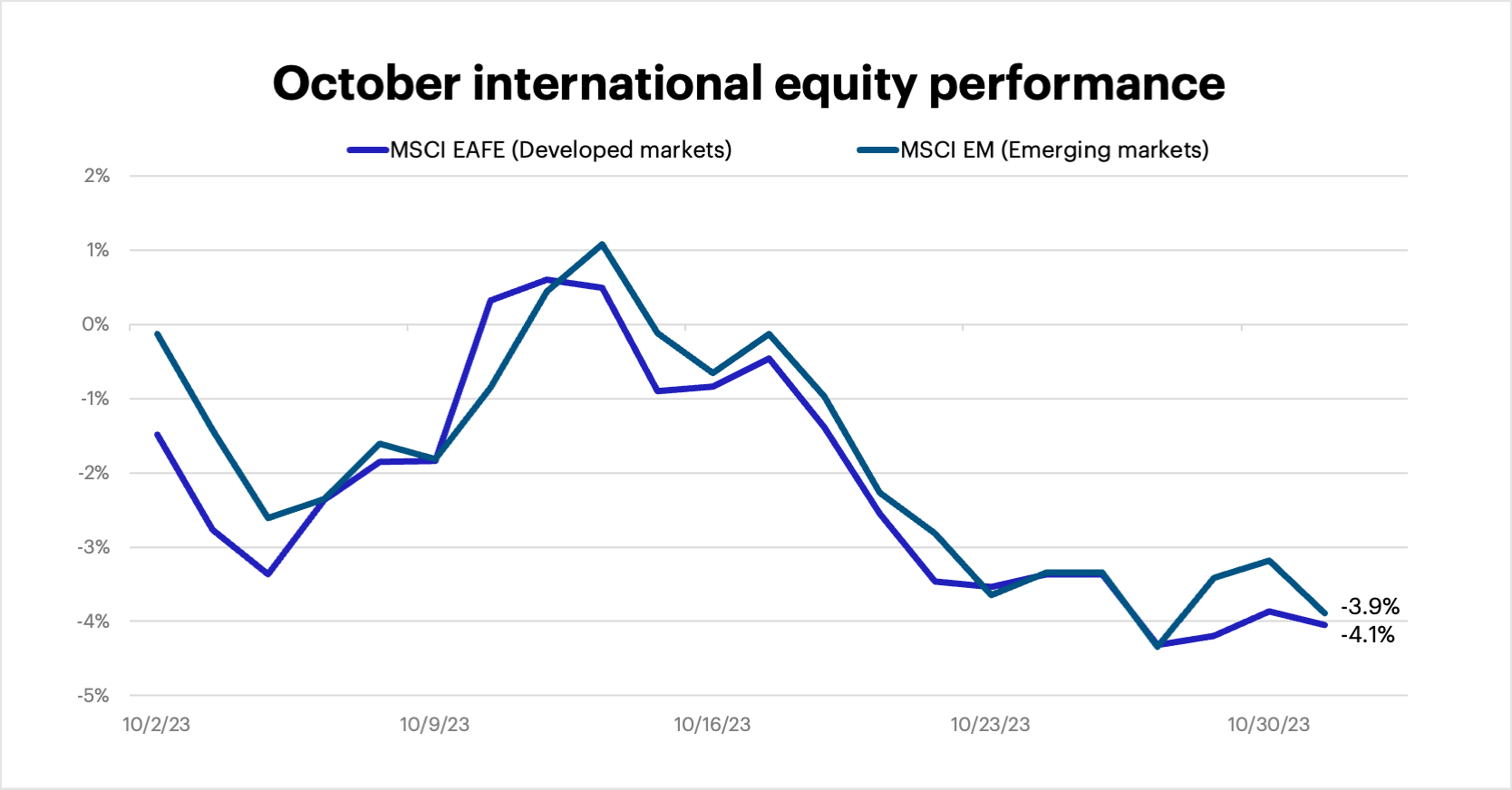

International equities

Global stocks underperformed the S&P 500 in October, with developed and emerging markets posting comparable losses. The MSCI EM Index of emerging markets fell 3.9%, while the MSCI EAFE Index of developed markets lost 4.1%:

FactSet Research Systems (It is not possible to invest in an index.)

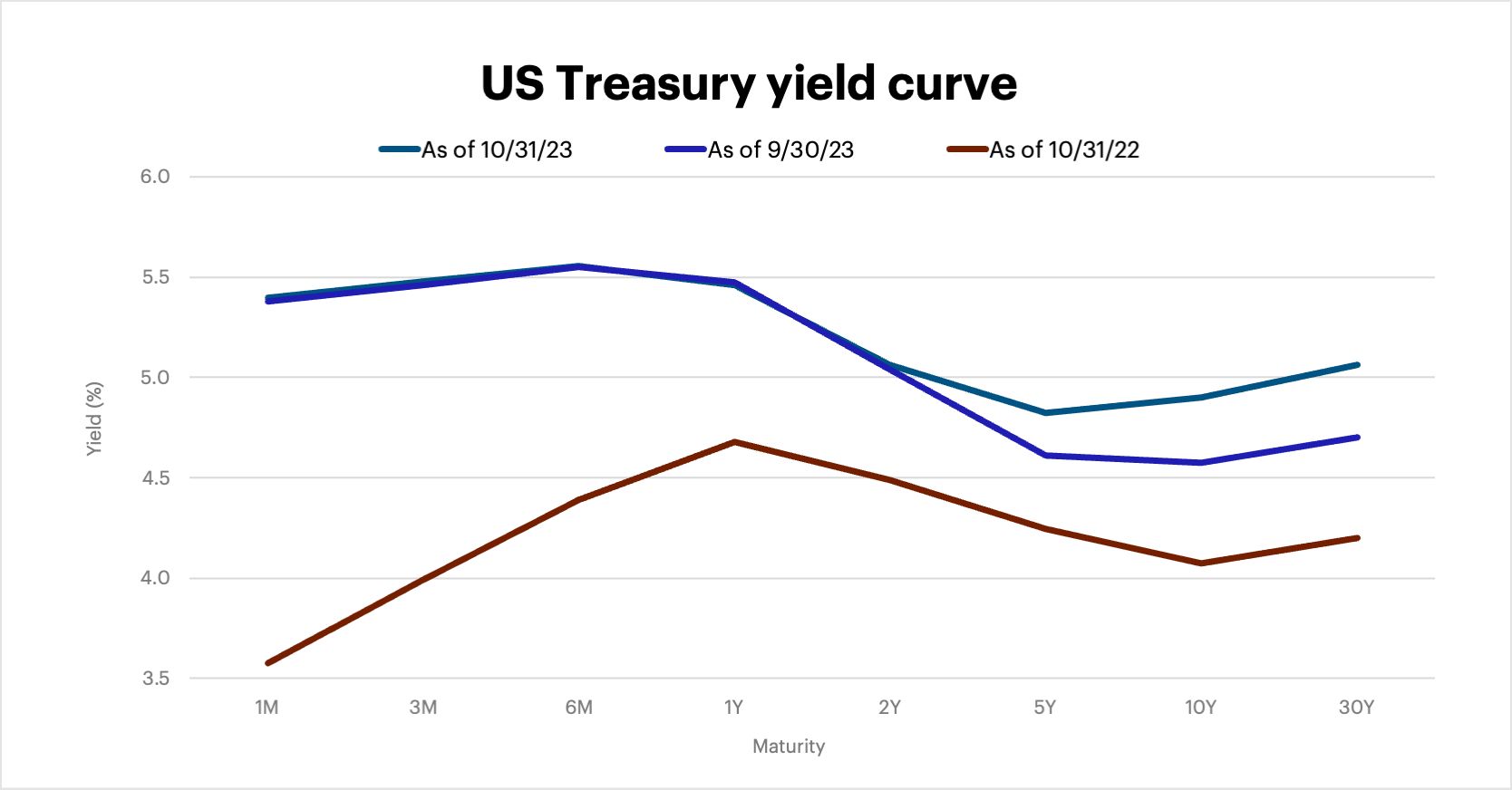

Fixed income

Bond prices extended their sell-off in October as yields continued to climb, mostly at the long end of the curve. (Morgan Stanley & Co. analysts highlighted one possible development from higher long-term yields: tighter financial conditions that increase the likelihood of an economic slowdown, making the Fed less hawkish.1) The benchmark 10-year Treasury yield rose for the sixth-straight month, ending October at 4.9%, up from 4.57% at the end of September:

FactSet Research Systems

Looking ahead

A few thoughts as we head into a new month:

- High rates and fixed income. The Fed may not have raised rates today, but that doesn’t change the primary market theme: Higher interest rates aren’t going away any time soon. But remember that the upside of high rates is meaningful fixed income returns—better than they have been in more than 15 years.

- Tune out negative sentiment. Last month brought war in the Middle East and political turmoil on Capitol Hill. This month ushers in (again) the possibility of a government shutdown. Negative sentiment stemming from uncertainty and volatility is always part of the markets, but investors shouldn’t let it distract them from their long-term goals.

- That’s why they’re called “cyclicals.” Many cyclical investments, such as small-cap stocks, have been challenged in recent weeks. Although selling underperforming areas of a portfolio may satisfy the strong psychological need to “do something” in stressful times, these investments can provide important diversification. No one knows when they may turn around, and investors can’t reap their potential benefits if they abandon them.

This may not be an easy time for investors, but those who stay the course are usually the ones still standing when conditions improve. As always, stay disciplined, diversified, and focused on the long term.

Thanks for reading, and we’ll talk to you again next month.

Head of Portfolio Construction for Morgan Stanley Portfolio Solutions

Mike Loewengart is Head of Portfolio Construction for Morgan Stanley Portfolio Solutions and a Managing Director in the Morgan Stanley Wealth Management Global Investment Office. Mike is responsible for the asset allocation and investment vehicle selections used in E*TRADE from Morgan Stanley’s advisory platforms. Prior to joining E*TRADE in 2007, Mike was the Director of Investment Management for a large multinational asset management company, where he oversaw corporate pension plan assets. Early in his career, Mike was a research analyst focusing on investment manager due diligence for the consulting divisions of several high-profile investment firms. Mike holds series 7, 24, and 66 designations, as well as the Chartered Alternative Investment Analyst (CAIA) designation. He is a graduate of Middlebury College with a degree in economics.

Executive Director, Morgan Stanley WM Global Investment Office

Andrew Cohen is an Executive Director in the Morgan Stanley Wealth Management Global Investment Office. Prior to joining E*TRADE in 2014, he was the Director of Investments and Operations for a large Registered Investment Advisor, where his responsibilities included investment manager research, asset allocation, and portfolio construction. Previously, he was a Senior Research Analyst and Team Leader for Morgan Stanley. He is a CFA® charterholder and a member of the CFA Institute and CFA Society New York. He is a graduate of Virginia Tech with a Bachelor of Science (B.S.) in finance.

1 Morgan Stanley.com. Implications of the Treasury Market Sell-off. 10/25/23.

Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectors and companies. Technology stocks may be especially volatile. Risks applicable to companies in the energy and natural resources sectors include commodity pricing risk, supply and demand risk, depletion risk and exploration risk. Health care sector stocks are subject to government regulation, as well as government approval of products and services, which can significantly impact price and availability, and which can also be significantly affected by rapid obsolescence and patent expirations.

Yields are subject to change with economic conditions. Yield is only one factor that should be considered when making an investment decision.