A quick lesson in time decay

- All options lose value over time

- This “time decay” accelerates as expiration approaches

- Effect can work in your favor with short options positions

They say the only certainties in life are death and taxes, but options traders know there’s another: time decay.

One of the reasons traders sometimes prefer to sell options instead of buy them—regardless of their outlook—is that all options lose value over time. It’s a simple reflection of the reality that, because options have finite lifespans, each day that passes until expiration decreases the odds the option will have any value.

You don’t need to understand options-pricing models or the “Greeks” to get a handle on how time decay works. Consider a stock that’s trading at $75 that has a $100 call option expiring one year from now. Even though the option is well out of the money (above the current stock price), 12 months is plenty of time for it to rally $25, so the option will likely have a fair amount of time value reflected in its premium—that is, it will be more expensive than, say, a $100 call expiring in one month.

Taking this line of thought to its extreme, consider a $100 call on the same stock expiring in one day. The odds of the stock being able to mount the same rally in a single trading session are dramatically lower, so the option will have little, if any, time value. (Note: Time value, technically, also reflects the level of volatility—higher volatility usually results in higher options prices, and vice versa.)

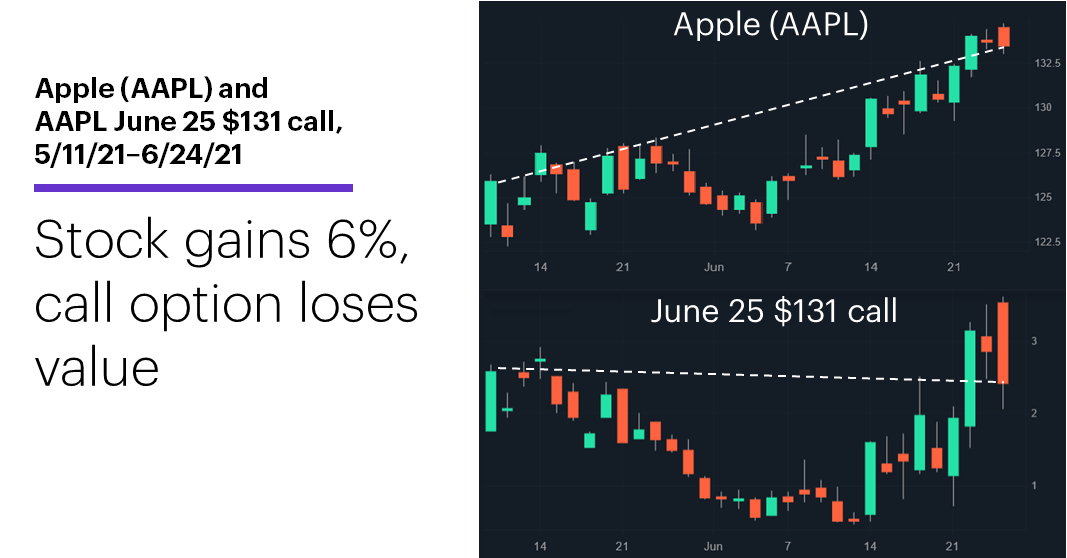

The following chart shows what this can look like in the real world. It shows Apple (AAPL) stock (top) with a $131 AAPL call option that expired on Friday. On May 11, AAPL closed at $125.91 and the $131 call closed at 2.57. As of last Thursday, APPL had rallied 6% to $133.41, but the $131 call closed lower, at 2.41:

Source: Power E*TRADE

That means on May 11, when the $131 call had no intrinsic value (the difference between the strike price and the stock price), its 2.57 premium consisted entirely of time value. By last Thursday, though, the time value had entirely disappeared, since the option’s price consisted entirely of its intrinsic value ($133.41–$131=2.41).

That’s time decay in a nutshell.

There’s one other “certainty” associated with time decay: All else being equal, it accelerates as expiration approaches—so, for example, the typical option will lose much more time value in the final five days of its life than in a five-day period six months before expiration.

The drawbacks of time decay can work in the favor of short options positions, especially in cases where premiums are also inflated because of high implied volatility (IV). In these situations, a short option can lose value on two fronts, as IV recedes to more normal levels and time decay marches on.

That’s why some traders like to sell high-IV options that are closer to expiration, and buy low-IV options with plenty of time before they expire.

When something’s avoidable, like time decay, it’s a good idea to understand how to avoid its negatives and potentially benefit from its positives.

Today’s numbers include (all times ET): S&P/Case-Shiller Home Price Index (9 a.m.), FHFA Housing Price Index (9 a.m.), Consumer Confidence (10 a.m.).

Today’s earnings include: AeroVironment (AVAV), National Beverage (FIZZ), FactSet (FDS).

Today’s IPOs include: Xometry (XMTR), SentinelOne (S), LegalZoom (LZ), Intapp (INTA), Integral Ad Science (IAS).

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.