Breaking down the types of structured investments

Morgan Stanley Wealth Management

11/25/25Summary: Structured investment products can be divided into four basic categories, each offering features designed for specific objectives.

Structured investments offer access to formula-based returns tailored to a particular market outlook. They provide exposure to the performance of an underlying asset—such as equity indexes, equity securities, baskets of securities, commodities, or currencies—without ownership of that asset.

Let’s break down four common structured investment strategies:

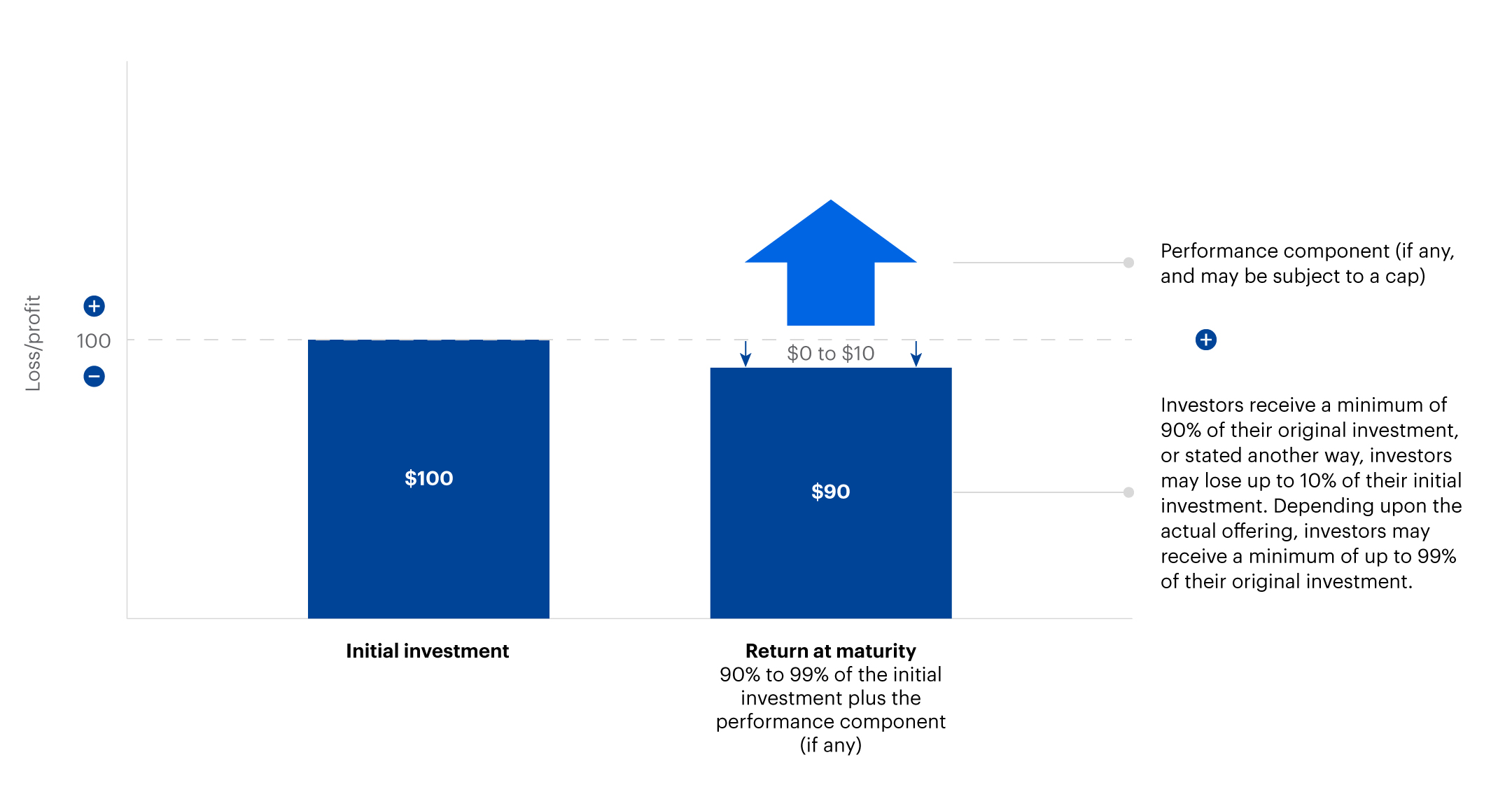

Partial principal at risk securities

Partial principal at risk securities are products structured to return between 90% and 99% of the initial investment principal at maturity, subject to the credit risk of the issuer. They are issued as notes and are not insured by the FDIC. These securities usually don’t make interest payments, but instead offer the potential for an investor to earn a supplemental payment at maturity based on the performance of the underlying asset. However, there may be a cap or other feature that limits the return at maturity.

These securities may be appropriate for investors who:

- Are willing to forgo a fixed coupon payment, and potentially have no return, or up to a 10% loss of principal in exchange for potentially higher returns through exposure to underlying assets.

- Have a less aggressive investment strategy or want to manage overall principal at risk.

- Are looking to preserve their initial investment at maturity, with some potential for capital appreciation.

They may not be appropriate for investors who:

- Want to avoid exposure to the credit risk of issuers of structured notes.

- Are seeking regular interest or dividend payments.

- Don’t want their returns to be capped.

- Require investments with a liquid secondary market.

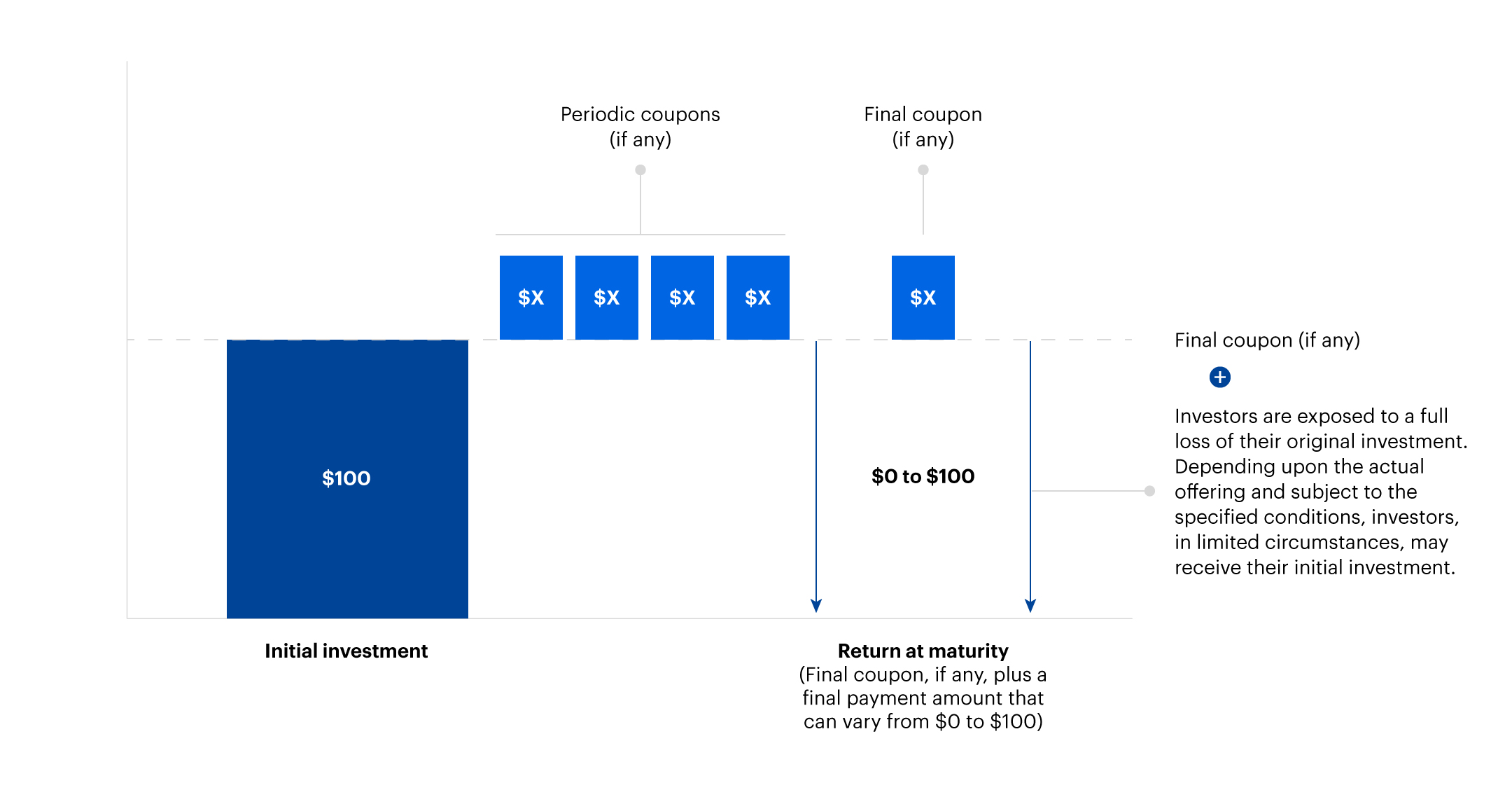

Enhanced yield investments

Enhanced yield investments encompass a variety of products that may provide regular income derived from exposure to the performance of underlying assets. But here’s the catch: In exchange for the potential to earn above-market payments, or yields, investors may be exposed to the risk of a complete loss of principal.

These investments may be appropriate for investors who:

- Are willing to risk the loss of some or all of their principal in exchange for above-market yields, which in some cases may be dependent upon the performance of the underlying asset.

- Have a neutral to moderately bullish view on underlying asset or assets.

- Are willing to forgo returns based on any appreciation of the underlying asset.

These investments may not be appropriate for investors who:

- Want to avoid exposure to the credit risk of issuers of structured investments.

- Are looking for regular periodic payments.

- Require a guaranteed payment at maturity.

- Want to participate in the appreciation of an underlying asset.

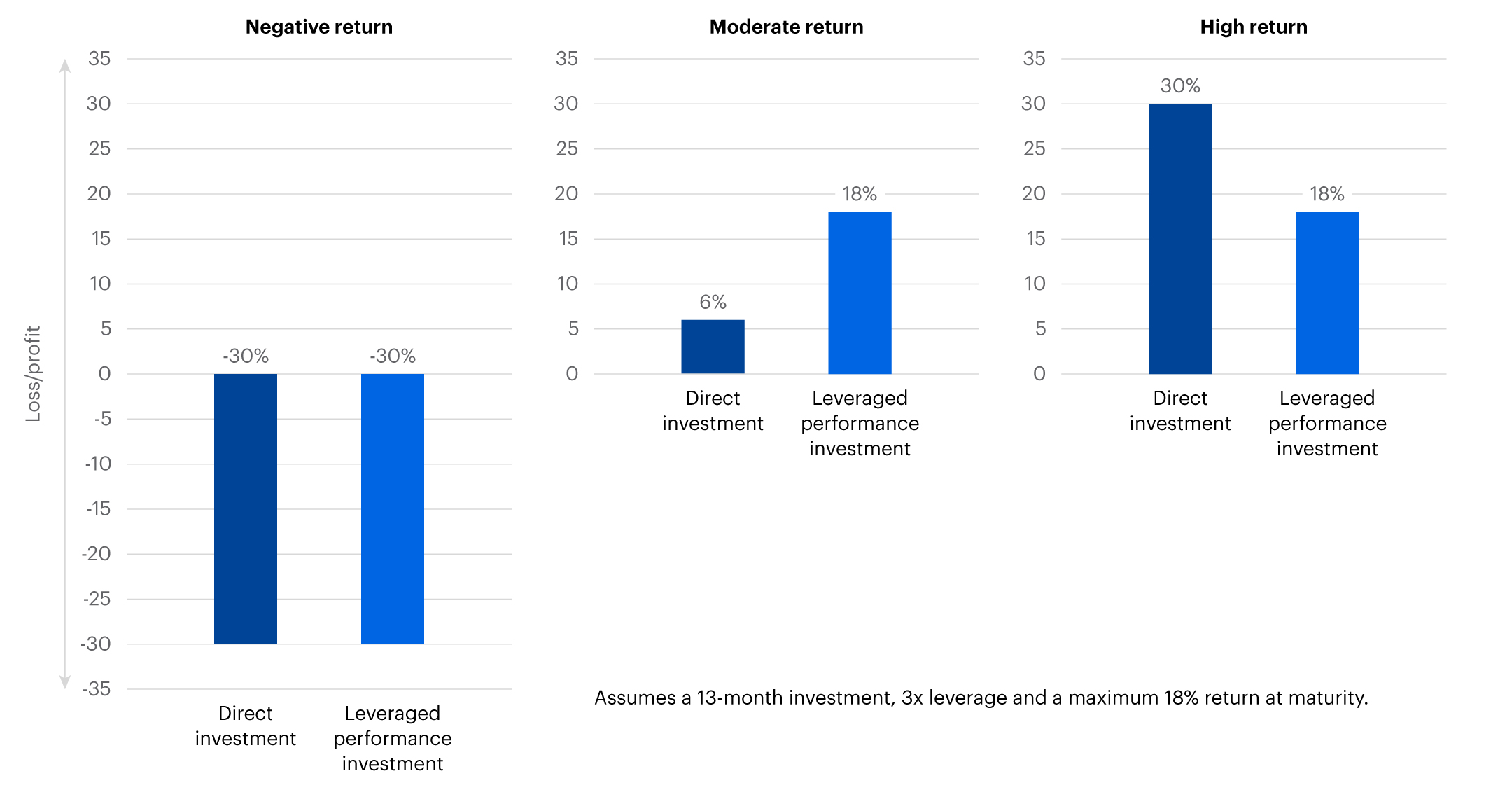

Leveraged performance investments

Leveraged performance investments attempt to generate enhanced returns relative to an underlying asset’s actual returns within a certain range of performance, and they are usually subject to a cap. However, in exchange for the potential to achieve excess returns within the defined range, most leveraged performance securities expose investors to the potential loss of some or all of their principal.

These investments may be appropriate for investors who:

- Are interested in generating returns beyond those available in moderately rising or range-bound markets.

- Can take on full or partial downside risk and are able to tolerate a partial or total loss of principal.

- Seek to diversify their portfolio by gaining exposure to a variety of underlying asset classes.

- Are willing to accept an investment with a maximum payout at the time of maturity.

They may not be appropriate for investors who:

- Want to avoid exposure to the credit risk of issuers of structured investments.

- Require interest or dividend payments.

- Are unwilling to accept a loss of any principal.

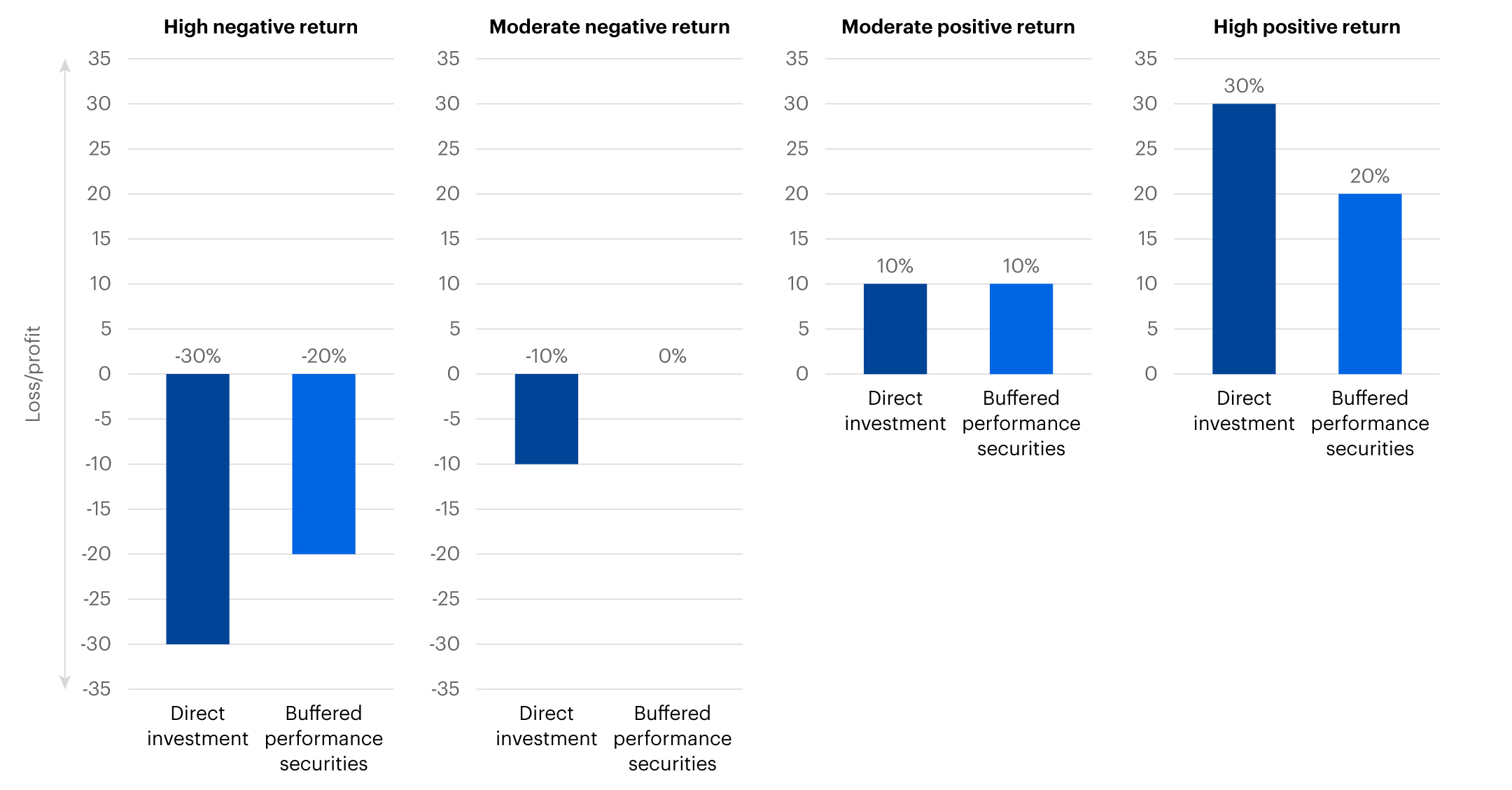

Access investments

As the name suggests, these investments provide “access” to the returns of a sector, asset class, or investment strategy that might be difficult to achieve via a direct investment. For example, investors may seek exposure to a basket of foreign currencies relative to the performance of the US dollar. This type of structured investment usually attempts to mirror the performance of the underlying asset(s) and can be tied to both negative and positive returns.

The following illustrations show the returns, at maturity, of a hypothetical buffered performance security where investors have 1:1 upside exposure to the positive performance of an equity basket, but also have a buffer against loss of the first 10% decline in the value of the basket with 1:1 downside exposure (principal losses) thereafter.

Access investments may be appropriate for investors who want exposure to assets beyond traditional US markets. But these investments may not be appropriate for investors who:

- Want to avoid exposure to the credit risk of issuers of structured investments.

- Want to receive interest or dividend payments.

- Desire uncapped returns or returns that correspond to a direct investment in a single underlying asset.

Structured investments can help investors across a range of risk-return objectives, but it’s important to carefully read the prospectus. Learn more about some of the risks inherent in structured investments before getting started.

CRC# 4981189 11/2025