Stocks weigh economic signals

- Market dips amid latest signs of economic strength

- Oil gushes to fresh highs, precious metals retreat

- This week: Inflation (CPI and PPI), retail sales

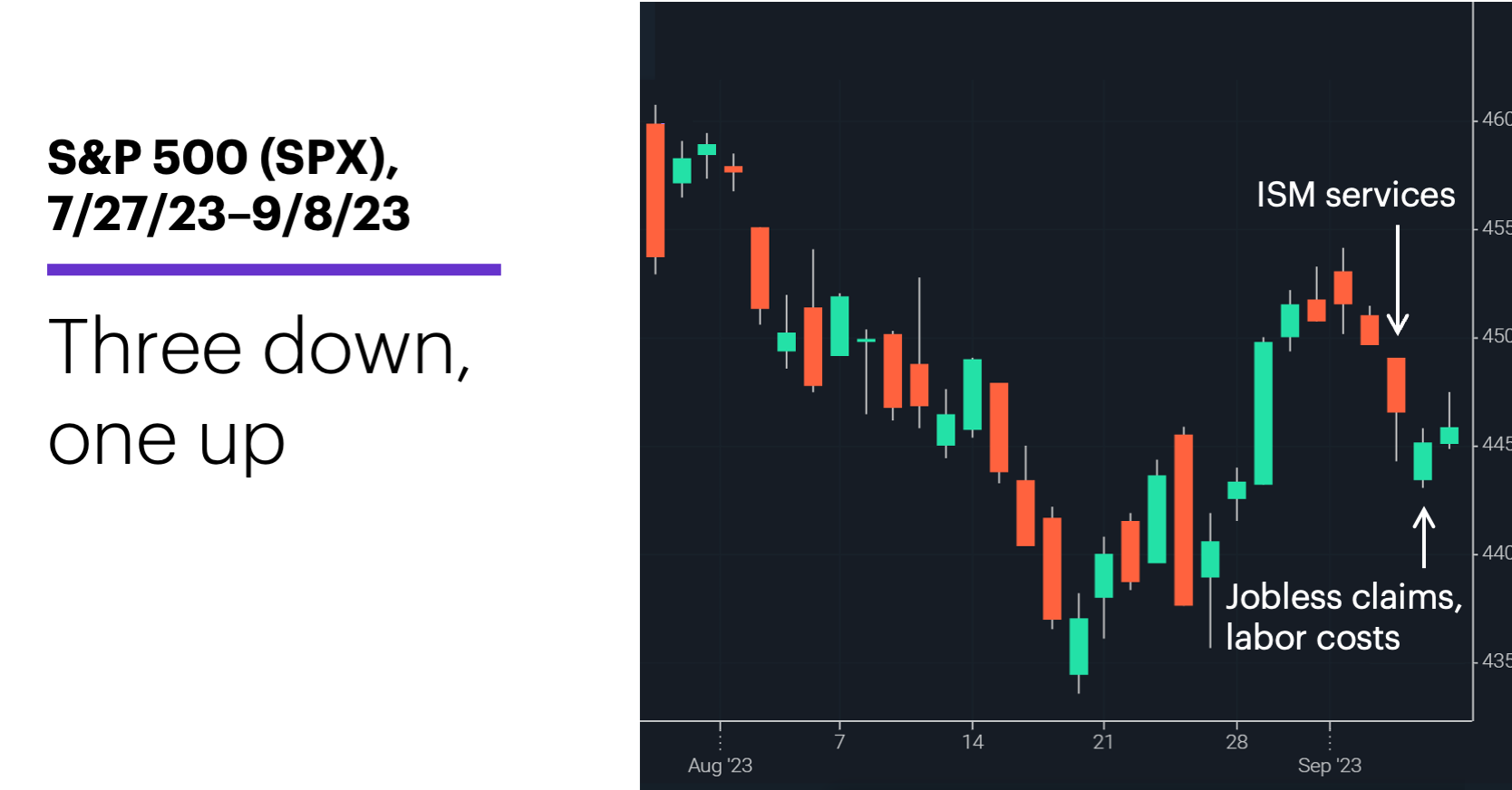

After closing out a bearish August with an up week, stocks went in the other direction to start September.

The S&P 500 (SPX) bounced off its Thursday lows and eked out a small gain on Friday, but still lost ground for the fourth week out of the past six:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Slippery start to September.

The fine print: The market’s reaction to last week’s numbers may have had a “good news is bad news” component. After the ISM Services index topped estimates on Wednesday, jobless claims surprised to the downside on Thursday, while labor costs jumped unexpectedly—all highlighting economic resilience that could keep the Fed hawkish and interest rates high.

The number: 35. Last week was the 35th time in the past 67 years that the US stock market declined in the shortened week following Labor Day.

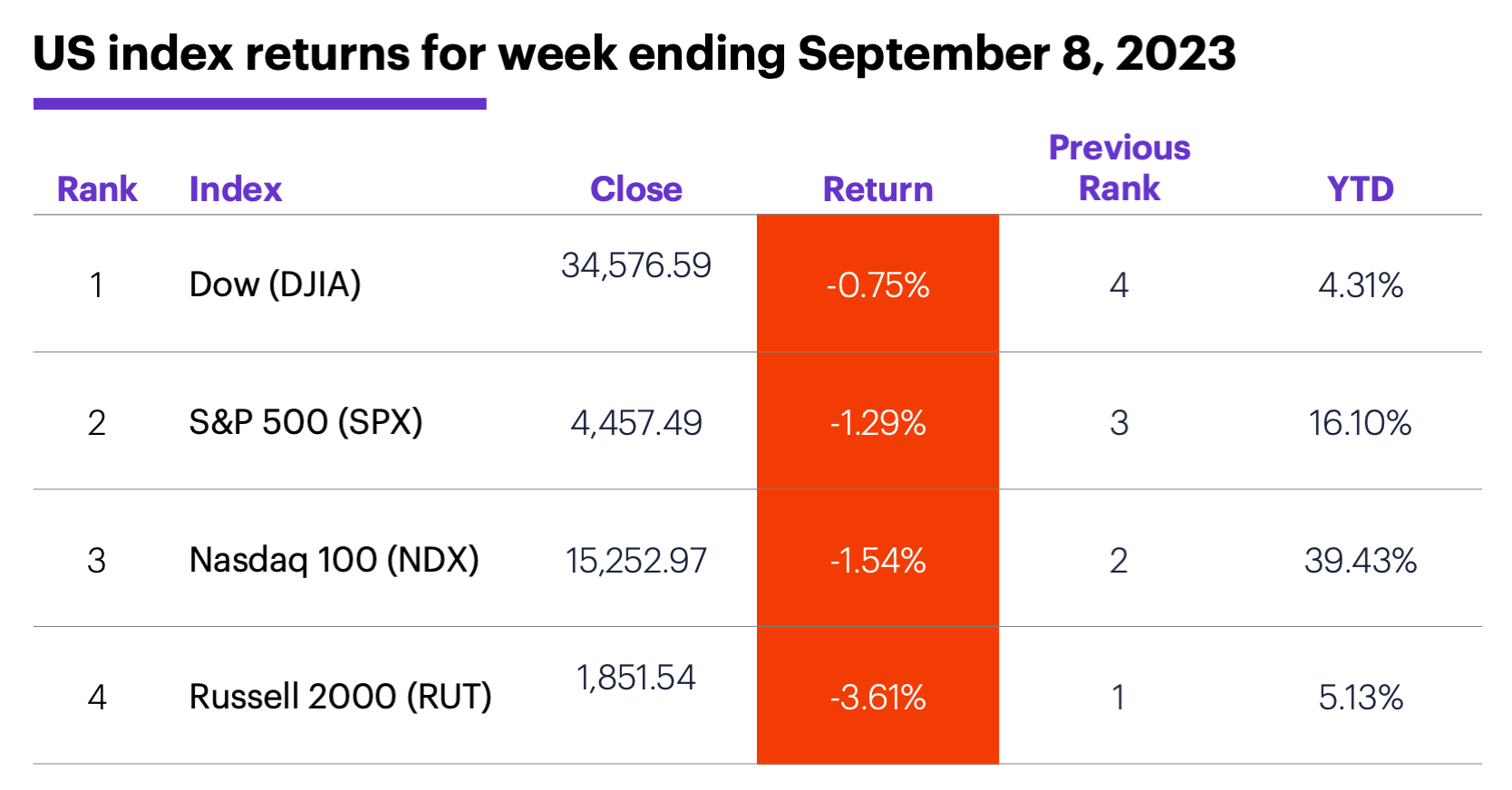

The scorecard: Just as it led the US market to the upside a week earlier, the small-cap Russell 2000 (RUT) lost the most ground last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were energy (+1.4%), utilities (+0.9%), and financials (-1.1%). The weakest sectors were materials (-0.8%), tech (-2.3%), and industrials (-2.9%).

Stock movers: Designer Brands (DBI) +22% to $12.66 and G-III Apparel (GIII) +24% to $23.98, both on Thursday. On the downside, Overstock (OSTK) -23% to $20.99 on Wednesday, VinFast Auto (VFS) -27% to $17.99 on Thursday.

Futures: October WTI crude oil (CLV3) closed at $87.54 last Wednesday—as high as the market has been since November 11—then held steady to end the week at $87.51. December gold (GCZ3) retreated last week, closing Friday near a two-week low of $1,942.70.

Coming this week

Inflation data—the CPI and PPI—dominate the economic calendar, but expect the United Auto Workers (UAW) strike threat to get plenty of attention as long as it goes unresolved:

●Monday: Consumer Inflation Expectations

●Tuesday: NFIB Business Optimism Index

●Wednesday: Consumer Price Index (CPI)

●Thursday: Producer Price Index (PPI), Retail Sales, Business Inventories

●Friday: Import and Export Prices, Empire State Manufacturing Index, Industrial Production, Capacity Utilization, Consumer Sentiment (prelim)

This week’s earnings include:

●Monday: Oracle (ORCL), Casey’s General Stores (CASY)

●Wednesday: Cracker Barrel (CBRL)

●Thursday: Adobe (ADBE), Lennar (LEN)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Capital and the Capitol

Last week’s return of Congress from summer break launched what could be a busy season of legislative debate on a wide range of issues affecting investors, including tech and artificial intelligence regulation, and defense spending.

But as Morgan Stanley & Co. analysts note, the most important issue may be the risk of a government shutdown at the end of September if Capitol Hill can’t come to an agreement on spending levels for next year.1 As the analysts explain, while a shutdown itself wouldn’t necessarily derail the prospect of a soft landing for the economy, it would introduce an element of risk into the Q4 economic picture.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Congressional Return Raises Question for Markets. 9/6/23.