Stock bounce follows through

- Stocks gain despite sticky inflation, geopolitical turmoil

- Oil and gold jump, small caps retreat

- This week: Earnings, retail sales, housing

A week that began with the market building on its October 6 rally ended on a more cautious note amid geopolitical uncertainty, inflation concerns, and the beginning of earnings season.

The S&P 500 (SPX) hit its highest level since September 20 early last Thursday before pulling back the remainder of the week—despite an early bump on Friday following solid numbers from the first banks to report Q3 earnings:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Market climbs as earnings season begins.

The fine print: While the core CPI and PPI readings declined month over month, both inflation barometers were a little hotter than anticipated. The overall picture remained one of stubborn inflation and continued economic strength—and, by implication, high interest rates.

The number: 5, how many weeks Congress has to avoid a government shutdown on November 17 (see “Vacancy in the House,” below).

The move: While the Cboe Volatility Index (VIX) usually declines when the SPX rallies, last week the VIX closed higher—a possible indication the options market expects more near-term volatility despite the stock market bounce.

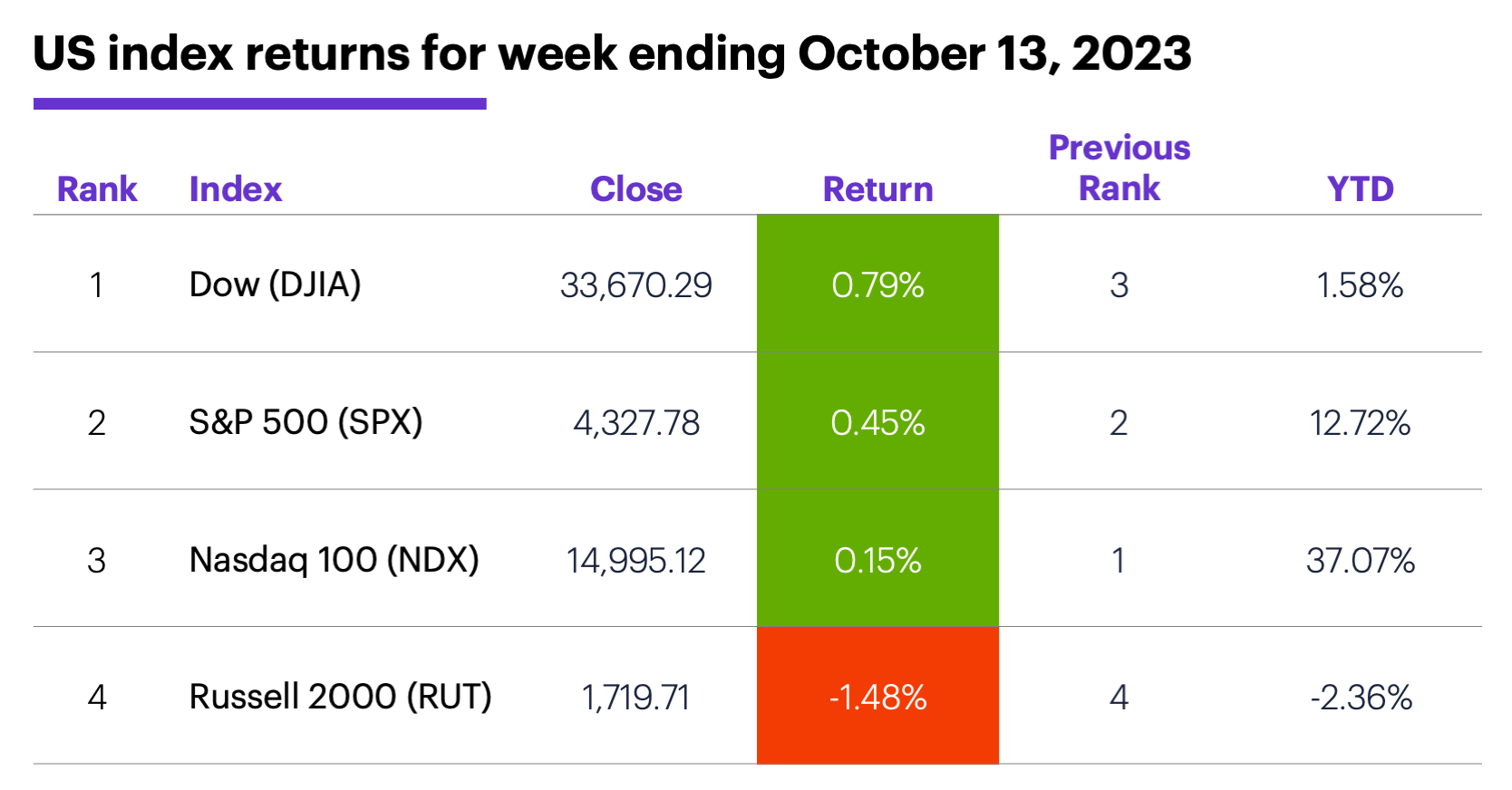

The scorecard: The major US indexes had modest gains last week—except for the small cap Russell 2000 (RUT), which lost ground and remained underwater for the year:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were energy (+4.4%), utilities (+3.6%), and real estate (+2.2%). The weakest sectors were consumer discretionary (-0.7%), materials (-0.5%), and communication services (-0.3%).

Stock movers: PGT Innovations (PGTI) +22% to $31.95 on Tuesday, Revolution Medicines (RVMD) +24% to $29.91 on Friday. On the downside, Akero Therapeutics (AKRO) -63% to $18.15 on Tuesday, T2 Biosystems (TTOO) -53% to $8.20 on Friday.

Futures: December WTI crude oil (CLZ3) ended a volatile week up more than $5 at $86.35. The market rallied more than 4% last Monday and more than 5% on Friday—the first time oil has gained 4% or more on two days in the same week in more than a year. December gold (GCZ3) logged its biggest up week since March, ending the up more than $95 at $1,941.50. Week’s biggest gains: November heating oil (HOX3) +9.1%, November VIX (VXX3) +8.2%. Week’s biggest losses: December oats (ZOZ3) -9.6%, October Micro ether (ETHV3) -6.5%.

Coming this week

The first full week of earnings season is heavy on banks and other financials, but it also includes high-profile names from other sectors, including pharma, tech, consumer staples, and airlines:

●Monday: Enerpac (EPAC), FB Financial (FBK)

●Tuesday: Bank America (BAC), Bank New York Mellon (BK), Goldman Sachs (GS), Johnson & Johnson (JNJ), Lockheed Martin (LMT), United Airlines (UAL), Wintrust (WTFC)

●Wednesday: Abbott Labs (ABT), Morgan Stanley (MS), Procter and Gamble (PG), US Bancorp (USB), Alcoa (AA), Discover (DFS), Lam Research (LRCX), Netflix (NFLX), Tesla (TSLA)

●Thursday: American Airlines (AAL), Freeport-McMoRan (FCX), Fifth Third Bank (FITB), AT&T (T), Taiwan Semiconductor (TSM), CSX (CSX), Intuitive Surgical (ISRG), WD-40 (WDFC)

●Friday: American Express (AXP), Schlumberger (SLB)

This week’s numbers include:

●Monday: Empire State Manufacturing Index

●Tuesday: Retail Sales, Industrial Production, Capacity Utilization, Business Inventories, NAHB Housing Market Index, Retail Inventories (ex-autos)

●Wednesday: Housing Starts and Building Permits, Fed Beige Book

●Thursday: Existing Home Sales, Leading Indicators Index

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Vacancy in the House

One story that lost a little traction last week was domestic politics. With a possible government shutdown looming in mid-November, House Republicans unable to decide on a new Speaker, and an election year about to get into full swing, investors may want to temper their expectations of market-positive developments emerging from Washington for the time being.

As Morgan Stanley & Co. analysts note, Congress is unlikely to deliver any significant legislation between now and the 2024 election, aside from (hopefully) the funding bills required to keep the government open. Despite the possible advantages of deadlocked government for corporations, such as fewer regulatory and tax burdens, an absence of legislative initiatives also means limited fiscal spending—and that implies potential headwinds for stocks, given the contribution government spending has arguably made to the stock market’s gains.1

And while the analysts don’t necessarily think the current Capitol Hill dysfunction represents an immediate or top-level threat to the market, they also point out that could change, and at the very least, it doesn't foster investor confidence in the US growth trajectory.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Signals from the Speaker of the House Vacancy. 10/11/23.