Intraweek reversal

- Stocks swing as Fed stands pat and labor market cools

- Small caps and utilities rally, crude oil falls below $80

- This week: 1,500-plus earnings, Fed on speaking tour

Considering where the stock market was after last Tuesday’s closing bell, bulls had to be pretty happy with where things stood at the end of the week.

On April 30, the S&P 500 (SPX) wrapped up its weakest month since September with a 1.8% decline, and after Wednesday’s lower close, an up week was looking increasingly unlikely. But solid buying on Thursday and Friday—after a Fed policy meeting, an Apple (AAPL) earnings beat, and an unexpectedly soft monthly jobs report—erased the week’s losses:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation. Note: It is not possible to invest in an index.)

The headline: Traders glimpse light at the end of the interest rate tunnel, reverse pullback.

The fine print: After the Fed left interest rates unchanged last Wednesday, Chairman Jerome Powell negated the possibility of a rate hike, but also downplayed the idea of cuts in the face of stubborn inflation. Friday’s softer-than-expected jobs report may not have totally transformed that picture, but continued labor market weakness will make it easier for the Fed to pull out the scissors and start trimming.

The number: 175,000, the number of new jobs created in April, well below the 240,000 consensus estimate. Also, the unemployment rate ticked higher to 3.9%.

The move: After falling to its lowest levels vs. the US dollar since 1990, the Japanese yen gained 3.8% vs. the US dollar last week—its biggest up week since 2022—amid speculation the Bank of Japan stepped in to strengthen its currency.1 Morgan Stanley & Co. strategists recently discussed the implications of a stronger dollar on other currencies, particularly in Asia, and what the buck’s forward path may look like.

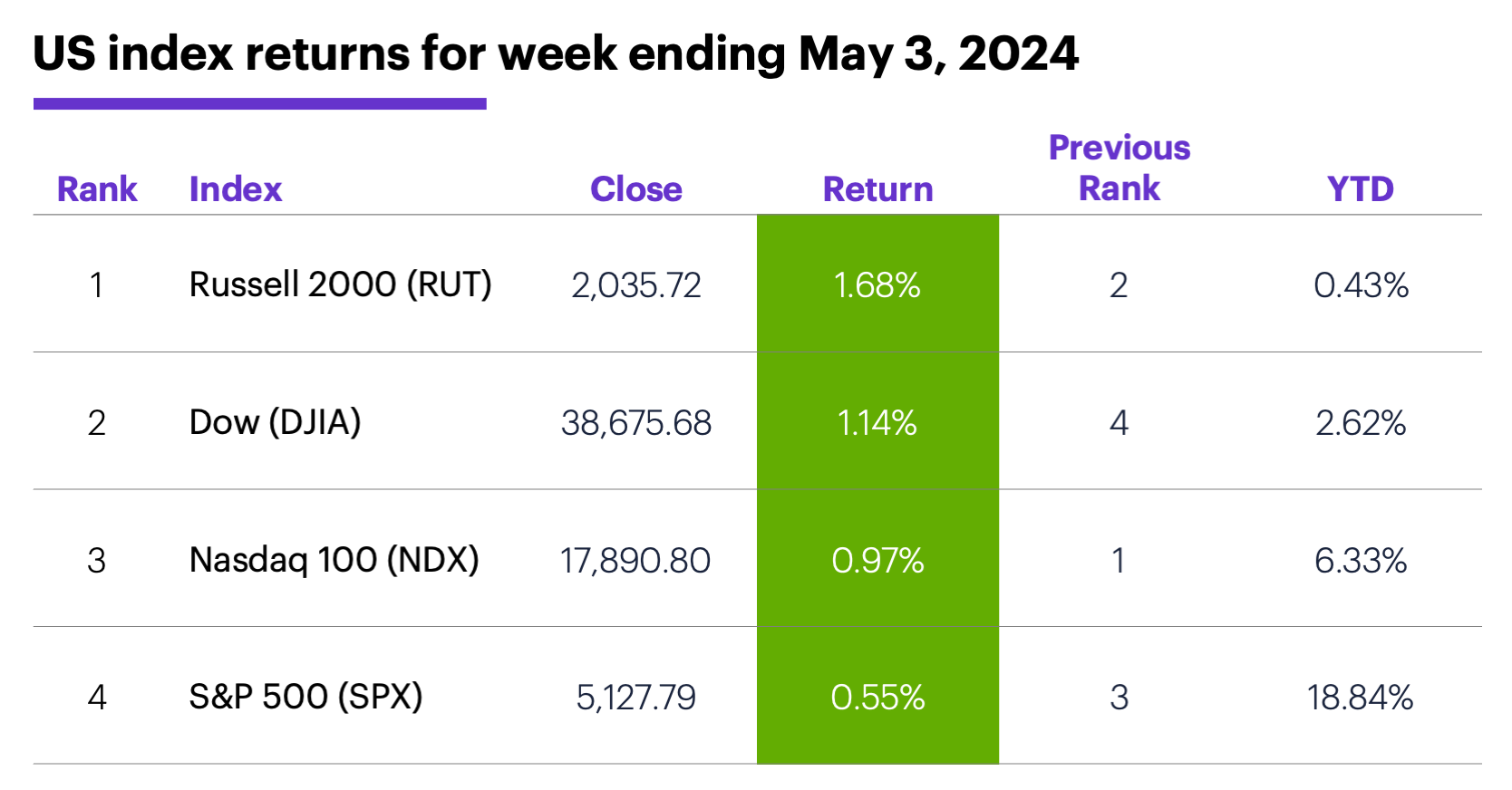

The scorecard: The Russell 2000 (RUT) small cap index led the market last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were utilities (+3.1%), consumer discretionary (+1.6%), and tech (+1.5%). The weakest sectors were energy (-3.6%), communication services (-0.6%), and financials (-0.6%).

Stock movers: Deciphera Pharmaceuticals (DCPH) +73% to $25.28 on Monday, Canopy Growth (CGC) +79% to $14.88 on Tuesday. On the downside, XPEL (XPEL) -39% to $32.86 on Thursday, Sprout Social (SPT) -40% to $28.82 on Friday.

Futures: The biggest down week since October for June WTI crude oil (CLM4) left the market nearly $6 lower at $78.11. June gold (GCM4) fell nearly $39 last week, closing Friday at $2,308.60. Week’s biggest gainers: June natural gas (NGM4) +12.1%, July soybean meal (ZMN4) +8%. Week’s biggest decliners: July cocoa (CCN4) -23.1%, July coffee (KCN4) -10.4%.

Coming this week

More than 1,500 companies will report during the busiest week of earnings season so far. A small sample:

●Monday: Axsome Therapeutics (AXSM), CRISPR Therapeutics (CRSP), Spirit Airlines (SAVE), Tyson Foods (TSN), Teradata (TDC), Vertex Pharmaceuticals (VRTX)

●Tuesday: Datadog (DDOG), Disney (DIS), WK Kellogg (KLG), Kenvue (KVUE), Rockwell Automation (ROK), UBS (UBS), Arista Networks (ANET), Electronic Arts (EA), Janux Therapeutics (JANX), Lyft (LYFT), Match Group (MTCH), Occidental Petroleum (OXY), Reddit (RDDT), Wynn Resorts (WYNN)

●Wednesday: Anheuser Busch InBev (BUD), Shopify (SHOP), Toyota (TM), Uber (UBER), Airbnb (ABNB), AppLovin (APP), Arm Holdings (ARM), Duolingo (DUOL), Exact Sciences (EXAS), Royal Gold (RGLD), Sunrun (RUN), SolarEdge (SEDG)

●Thursday: Beam Therapeutics (BEAM), Canadian Solar (CSIQ), Fiverr (FVRR), Hyatt Hotels (H), Roblox (RBLX), Spectrum Brands (SPB), Tapestry (TPR), Tower Semiconductor (TSEM), US Foods (USFD), Dropbox (DBX), Dillard's (DDS), Yelp (YELP)

●Friday: DigitalOcean (DOCN)

This week is light on economic data, heavy on Fed Speak:

●Monday: Richmond Fed President Tom Barkin speaks, New York Fed President Williams speaks

●Tuesday: Consumer Credit

●Wednesday: Wholesale Inventories, Fed Governor Lisa Cook speaks

●Thursday: Weekly Jobless Claims

●Friday: Consumer Sentiment (preliminary), Chicago Fed President Austan Goolsbee speaks

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Bucking the election year trend?

Market mover update: Kellanova (K) dipped on Friday, but only after a 7.6% Thursday rally broke the stock out of its choppy 2024 consolidation (see “Time frame price perspective”). Monster Beverage (MNST) tagged its highest level in nearly two weeks on Friday (see “Pre-earnings fizz”). Magna International (MGA) fell 3.6% on Friday after releasing earnings, but the tens of thousands of options that traded nearly two weeks ago were still on the books (see “Stock tests lows, options volume tests highs”).

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on X (Twitter), @ETRADE, for useful trading and investing insights.

1 CNBC.com. Japan’s yen had a roller coaster week amid suspected intervention. Here’s what you need to know. 5/3/24.