Notes from the markets

- Fed hikes, stock market slumps

- Options market still expecting bank volatility

- Oil slide continues, crude falls to five-week low

Stocks hovered in mildly positive territory early Wednesday following Tuesday’s sharp sell-off, but lost momentum after the Federal Reserve announced it would (as expected) raise interest rates for the 10th time since March 2022, pushing the benchmark Fed funds rate to a target range of 5%–5.25%—the highest it’s been since 2006.

The official statement removed language suggesting the Fed anticipated further rate hikes, although it didn’t close the door on that possibility. The S&P 500 (SPX), which was up roughly 0.3% immediately before the Fed’s announcement at 2 p.m. ET, was more or less unchanged an hour later, but subsequently drifted lower and ended the day in negative territory.

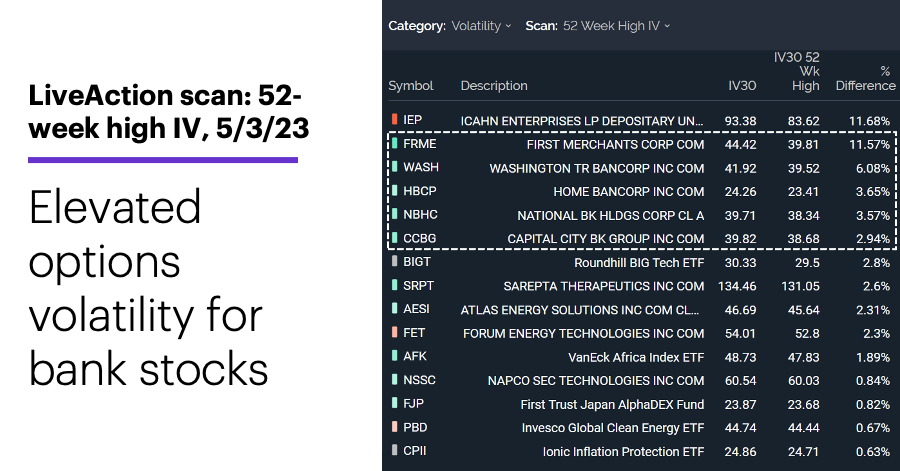

LiveAction hits: Anyone who thinks the bank story is no longer relevant may not have noticed how heavily represented bank stocks continue to be on multiple LiveAction scans—including Wednesday’s scan for 52-week high implied volatility. Five of the top six symbols yesterday morning were banks:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Market Mover Update: Crude oil’s sell-off continued yesterday, with June WTI oil futures (CLM3) following Tuesday’s 5.5% drop with a 5% intraday sell-off to $67.95—its lowest level since March 24.

For the second time in a week, Johnson Controls (JCI) sold off while experiencing heavier-than-average call options volume. On Wednesday morning the stock fell more than 1% after hitting a one-month intraday high of $60.45, and 750 contracts traded in both the May $60 and $65 calls.

Morgan Stanley: Did you know the tech sector has accounted for almost 85% of the S&P 500’s year-to-date gain? Traders wondering what’s been going on recently beneath the market’s (and the economy’s) surface may want to read “How Investors Can Prep for More Market Volatility” from Morgan Stanley Wealth Management, which highlights recent developments in market breadth, liquidity, and earnings.

Today’s numbers include (all times ET): Challenger Job-Cut Report (7:30 a.m.), International Trade in Goods and Services (8:30 a.m.), Weekly Jobless Claims (8:30 a.m.), Productivity and Costs (8:30 a.m.), EIA Natural Gas Report (10:30 a.m.).

Today’s earnings include: Datadog (DDOG), Hyatt Hotels (H), Kellogg (K), Lithium Americas (LAC), Martin Marietta (MLM), Moderna (MRNA), Intellia Therapeutics (NTLA), Vulcan Materials (VMC), Wayfair (W), XPO (XPO), Apple (AAPL), Booking Holdings (BKNG), Bumble (BMBL), Coinbase (COIN), Dropbox (DBX), Lyft (LYFT), Shopify (SHOP), Block (SQ).

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.