Market extends breakout

- Fed pauses, inflation cools, stocks march higher

- NDX rally hits new milestone, oil volatility drags down energy

- This week: Powell testimony, housing data, leading indicators

Traders and investors got what they were hoping for last week—evidence of cooling inflation. They also got what most of them expected—a pause in the Fed’s rate-hike cycle.

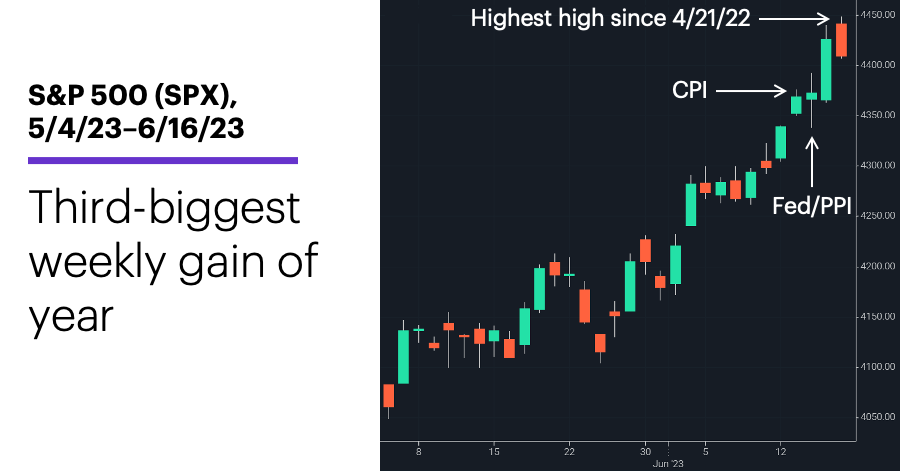

But they also got a bit of a surprise—a tough-talking Fed that suggested it may hike rates two more times before all is said and done. The market didn’t appear to be phased, though: The tech sector continued to fuel the rally, and the S&P 500 (SPX) pushed to its highest level since April 2022 before losing steam on Friday:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.) Note: It is not possible to directly invest in an index.

The headline: Broad market tags 10-month high.

The fine print: And it had tech to thank for it. The Nasdaq 100’s (NDX) 37.9% year-to-date gain through Friday was the tech index’s largest-ever return at this point in the year. The S&P 500 tech index ended last week up 41.2% for the year, while the PHLX Semiconductor Index (SOX)—fueled by a good deal of AI-inspired momentum—was up a 45.1%.

The number: 4%, the Consumer Price Index’s (CPI) year-over-year increase in May—below estimates, and down from 4.9% in April. The Producer Price Index (PPI) also came in lower than expected, highlighting slowing—but still high—inflation.

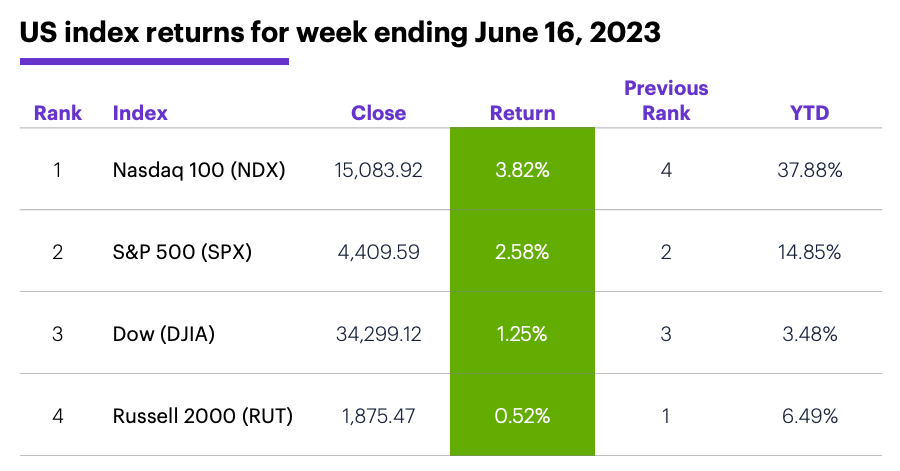

The scorecard: The Nasdaq 100 (NDX) tech index vaulted back to top of the index rankings last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were information technology (+4.4%), materials (+3.3%), and consumer discretionary (+3.2%). The weakest sectors were energy (-0.7%), real estate (+1.2%), and financials (+1.2%).

Stock movers: Chinook Therapeutics (KDNY) +58% to $37.98 on Monday, iRobot (IRBT) +21% to $51 on Friday. Cibus (CBUS) -29% to $16.41 and Methode Electronics (MEI) -18% to $36.99, both on Tuesday.

Futures: After closing at a three-month low of $67.51 last Monday, August WTI crude oil (CLQ3) bounced enough to end the week up more than $1.50 at $71.93. August gold (GCQ3) extended its trading range to three weeks, closing Friday down roughly $6 for the week at $1,971.20. Week’s biggest up moves: July natural gas (NGN3) +16.3%, July oats (ZON3) +12.8%. Week’s biggest down moves: June Micro ether (ETHM3) -6.3%, July milk (DCN3) -3.7%.

Coming this week

Fed Chair Jerome Powell’s Senate testimony on Thursday highlights the economic calendar:

●Monday: NAHB Housing Market Index (US markets closed for Juneteenth)

●Tuesday: Housing Starts and Building Permits

●Thursday: Current Account Q1, Fed Chairman Jerome Powell Senate testimony, Existing Home Sales, Leading Economic Indicators Index

●Friday: S&P Global Manufacturing and Service PMIs (flash)

This week’s earnings include:

●Tuesday: FedEx (FDX)

●Wednesday: Korn Ferry (KFY), Winnebago (WGO), Enerpac Tool (EPAC), KB Home (KBH)

●Thursday: Accenture (ACN), Darden Restaurants (DRI), FactSet Research (FDS)

●Friday: CarMax (KMX)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Roughly six months and 180 degrees later

The market landscape may appear very different than it did on January 1, but that may be leading some traders and investors to misjudge the current terrain.

While noting market sentiment had recently turned “outright bullish” recently amid the enthusiasm over all things AI, Morgan Stanley analysts point to a few signs the rally is potentially exhausting itself—including the contrarian observation several strategists and market commentators publicly proclaimed the end of the bear market.1 With sentiment and market positioning “180 degrees” from where they were at the beginning of the year, Morgan Stanley argues the market may not be properly prepared for the potential disappointment of weaker-than-expected earnings.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. A Historically Concentrated Market. 6/12/23.