Cautious start to H2

- Stocks slip—and so do bonds, as yields jump

- Jobs market still solid, but slower month over month

- This week: Inflation (CPI and PPI), earnings season kicks off

As traders get ready for this week’s inflation numbers and the beginning of another earnings season, the market will be attempting to bounce back from what has been a relatively rare event in recent weeks—a pullback.

Stocks rallied the first trading day of July, but the momentum didn’t last. The S&P 500 (SPX) posted just its second down week of the past eight as traders absorbed the latest employment data:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.) Note: It is not possible to directly invest in an index.

The headline: Stocks dip ahead of inflation reports.

The fine print: The market retreated after last Thursday’s strong ADP private payrolls number, and followed through on Friday even as the monthly jobs report came in much softer—but still not soft enough to change expectations for a rate hike later this month. Wednesday’s FOMC minutes showed three-quarters of Fed board members expected at least two more rate increases this year, and the probability of a July hike is currently above 90%.1

The number: 53.9, the ISM Services Index reading for June—well above expectations, highlighting the ongoing inflation pressures in the service economy. Below the headline, though, the data showed the prices paid by service businesses fell to their lowest level since March 20202—possibly a more hopeful sign on the inflation front.

The move: Bond yields jumped last week, with the yield on the benchmark 10-year T-note breaking out of its trading range to top 4% for the first time since March.

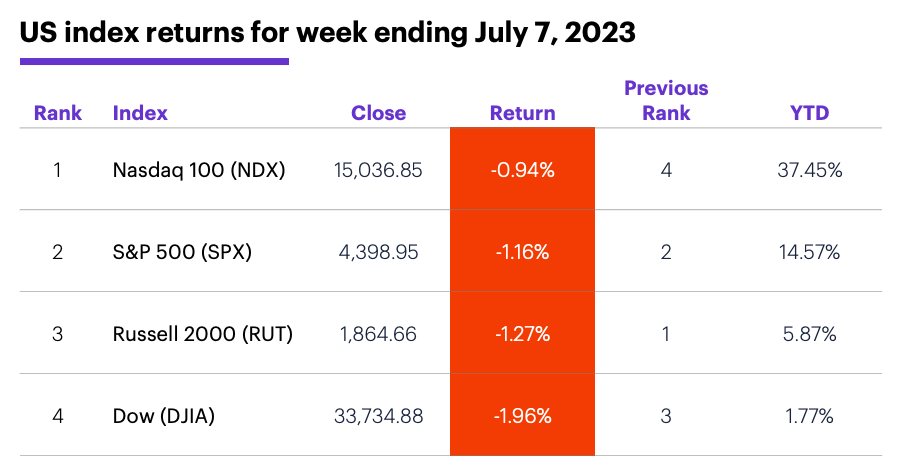

The scorecard: The Dow took the biggest step back:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector returns: The strongest S&P 500 sectors last week were consumer discretionary (+1%), utilities (+1%), and real estate (+0.7%). The weakest sectors were health care (-1.8%), materials (-1.1%), and industrials (-0.2%).

Stock movers: Cibus (CBUS) +22% to $15.51 on Thursday, Castle Biosciences (CSTL) +53% to $20.30 on Friday. On the downside, Consolidated Water (CWCO) -11% to $21.77 on Thursday.

Futures: A big Friday rally pushed August WTI crude oil (CLQ3) to its highest close ($73.86) since May 24. August gold (GCQ3) ended an aimless week slightly higher at $1,932.50.

Coming this week

Inflation data (CPI and PPI) highlight this week’s economic calendar:

●Monday: Wholesale Inventories, NY Fed Consumer Inflation Expectations, Consumer Credit

●Tuesday: NFIB Small Business Optimism Index

●Wednesday: Consumer Price Index (CPI), Fed Beige Book

●Thursday: Producer Price Index (PPI)

●Friday: Import Price Index, Consumer Sentiment

A new earnings season kicks off with big banks on Friday:

●Monday: PriceSmart (PSMT), WD-40 (WDFC)

●Wednesday: AngioDynamics (ANGO), MillerKnoll (MLKN)

●Thursday: Conagra (CAG), Cintas (CTAS), Delta Air Lines (DAL), Fastenal (FAST), PepsiCo (PEP), Progressive (PGR)

●Friday: Blackrock (BLK), Citigroup (C), JPMorgan Chase (JPM), UnitedHealth (UNH), Wells Fargo (WFC)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

AI and health care

Even though it contains biotech and other volatile industries, health care is usually considered a defensive sector. Recent history supports that view. Health care was the second-strongest S&P 500 sector in bear-dominated 2022, while it’s third from the bottom in what has, so far, been a bullish 2023.

While some traders and investors wouldn’t necessarily see the sector as fertile ground for AI-fueled advancement, Morgan Stanley & Co. analysts have highlighted the ways artificial intelligence and machine learning could alter the healthcare landscape, especially in the biotech space.3

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 CME Group (www.cmegroup.com). FedWatch Tool. 7/7/23.

2 Reuters. U.S. service sector picks up in June; inflation gradually slowing, ISM survey shows. 7/6/23.

3 MorganStanley.com. AI Opportunities in Healthcare. 7/6/23.