Traders crunch the numbers

- Stocks slip Friday, but push rally into February

- Traders buy rate hike, sell jobs report and tech earnings

- This week: Consumer sentiment, inflation expectations

It didn’t start or end well for bulls, but they still came out on top after an action-packed (and surprise-filled) week that included a Fed announcement, the monthly jobs report, and big-tech earnings.

The S&P 500 (SPX) stumbled last Monday and Friday, but its 4% surge in between—mostly after the Fed hiked interest rates on Wednesday—was enough to lock up its fourth up week out of the past five:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.) Note: It is not possible to directly invest in an index.

The headline: Stocks rally on rate hike, retreat on jobs and tech earnings.

The fine print: The market immediately embraced the Fed’s 0.25% rate hike, but sold off after Friday’s blowout employment report (see below) before recovering. Some investors and market watchers worry that a too-hot (read: inflationary) jobs market could prompt the Fed to continue raising interest rates.

The number: 517,000, the number of jobs the US economy added in January—nearly three times the expected total. Also, December’s figure was revised higher, from 223,000 to 260,000, and the unemployment rate unexpectedly fell from 3.5% to 3.4%. But the increase in average hourly wages—closely watched by inflation hawks—was in line with estimates at 4.4%, and down from 4.6% in December.

The moves: A day after Meta (META) jumped 23% after releasing earnings, Alphabet (GOOGL) and Amazon (AMZN) sold off after announcing their numbers, helping pressure the Nasdaq 100 (NDX) tech index—and the market as a whole—on Friday. Apple (AAPL) bucked that trend, pushing higher on Friday after some initial selling.

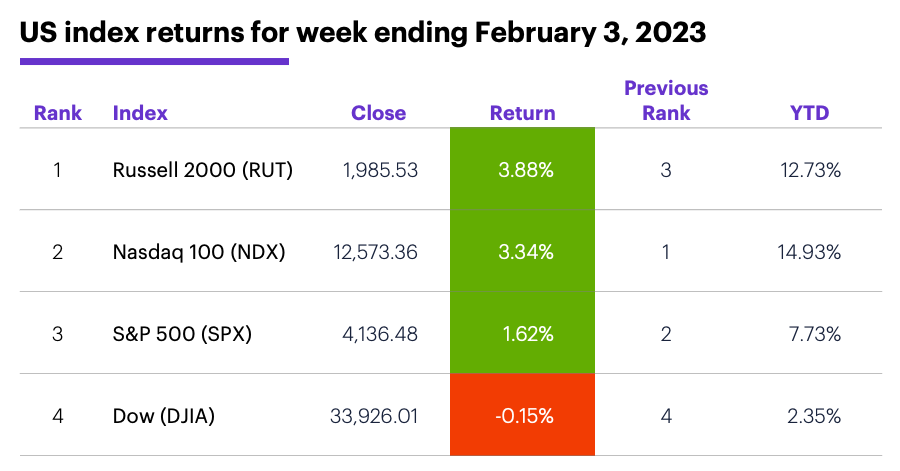

The scorecard: The Russell 2000 (RUT) small-cap index led the market last week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector roundup: The strongest S&P 500 sectors last week were communication services (+5.5%), information technology (+3.9%), and consumer discretionary (+2.2%). The weakest sectors were energy (-6%), utilities (-1.4%), and health care (-0.2%).

Stock movers: Wisa Technologies (WISA) +43% to $13.15 on Monday (then -20% to $10.49 on Tuesday), Atlas Technical Consultants (ATCX) +122% to $12.13 on Tuesday. On the downside, Dada Nexus (DADA) -16% to $12.78 on Monday, Canada Goose (GOOS) -24% to $18.81 on Thursday.

Futures: April gold (GCJ3) hit $1,975.20/ounce last Thursday—its highest level since April 2022—but reversed sharply to end the week at a three-week low of $1,876.60. March WTI crude oil (CLH3) also slid to its lowest price in three weeks, closing Friday at $73.39/barrel. Week’s biggest up moves: March orange juice (OJH3) +17.5%, March Dry Whey (DYH3) +7%. Week’s biggest down moves: March natural gas (NGH3) -15.5%, March heating oil (HOH3) -12.7%.

Coming this week

This week’s earnings include:

●Monday: Activision Blizzard (ATVI), ON Semiconductor (ON), Chegg (CHGG), Tyson Foods (TSN), Simon Property Group (SPG), Rambus (RMBS), Take-Two Interactive Software (TTWO)

●Tuesday: BP (BP), Fiserv (FISV), Incyte (INCY), Chipotle (CMG), Enphase Energy (ENPH), Illumina (ILMN), Paycom (PAYC), Vertex Pharmaceuticals (VRTX)

●Wednesday: CVS Health (CVS), Yum Brands (YUM), Mattel (MAT), O'Reilly Automotive (ORLY), Impinj (PI)

●Thursday: AbbVie (ABBV), Global Payments (GPN), Kellogg (K), PepsiCo (PEP), Ralph Lauren (RL), Lyft (LYFT), PayPal (PYPL), Verisign (VRSN)

●Friday: Mr. Cooper (COOP), Enbridge (ENB)

This week’s numbers include:

●Tueday: International trade deficit, Consumer Credit

●Wednesday: Wholesale Inventories

●Friday: Consumer Sentiment (preliminary)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

The view from the VIX seats

For much of Friday, the stock market appear to have trouble deciding what it wanted to do. After initially falling into a -1.2% hole, the index pushed into positive territory before falling to new lows later in the session.

One development on Thursday signaled such volatility was possible. While the SPX closed sharply higher on Thursday (+1.5%), so did the Cboe Volatility Index (VIX), which usually declines when the market rallies strongly:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

The VIX’s higher close on the day the SPX hit its highest high since last August suggested the options market was anticipating increased volatility, even though the market had pushed to the upside.

Since 1990, when the VIX closed up on a day the SPX gained 1% or more, the SPX closed higher the next day 50% of the time, but after three days it was lower 54% of the time with an average return of -0.2%.1

On a possibly related note, Morgan Stanley & Co. recently outlined its argument that the recent rally is likely a “bear trap” driven by fear of missing out (FOMO).2

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 Reflects 80 previous instances of the pattern, based on S&P 500 (SPX) and Cboe Volatility Index (VIX) daily prices, 1/2/90–2/3/22. Supporting document available upon request.. Supporting document available upon request.

2 MorganStanley.com. Fighting the Fear of Missing Out. 1/30/23.