Market absorbs geopolitical jolt

- Stocks erase most of week’s losses after tumbling on Russian invasion

- S&P 500 tests correction levels, Nasdaq enters/exits bear market

- This week: Jobs report, retail earnings, State of the Union

Traders and investors could have been excused for writing off last week as a lost cause not long after Thursday’s opening bell: Having already fallen four straight days, the S&P 500 (SPX) was quickly down more than 2.5% on the day and 5.4% for the week as the Russian–Ukraine standoff turned into an invasion.

But despite falling to its lowest level since last May, the SPX staged a dramatic intraday turnaround to end Thursday up more than 1.5%, and then tacked on another 2.2% on Friday to close higher for the week:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

The headline: Russian invasion jolts market—temporarily.

The fine print: The Thursday–Friday pivot amid the invasion story obscured a couple of the week’s more notable economic releases—a durable goods report that was more than three times stronger than analysts had estimated (+1.6% vs. +0.5%), and a PCE Price Index inflation reading that was high (+6.1% year over year), but in line with forecasts.

The number: 12. Counting last Thursday, that’s the number of times since 1985 that the Nasdaq 100 (NDX) has fallen 3% or more intraday and reversed to close up 3% or more. The last time it did it was in 2008.

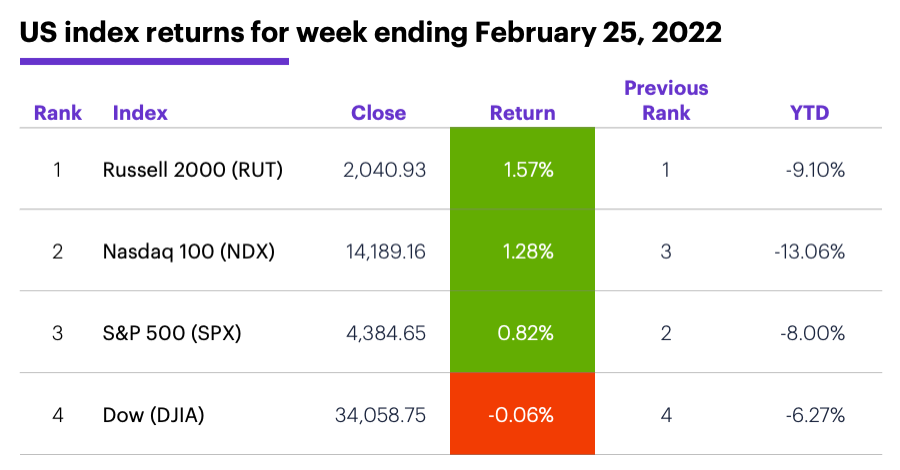

The scorecard: The small-cap Russell 2000 (RUT) extended its index leadership to a fourth week:

Source (data): Power E*TRADE. (For illustrative purposes. Not a recommendation.)

Sector roundup: The strongest S&P 500 sectors last week were real estate (+2.2%), health care (+1.9%), and utilities (+1.7%). The weakest sectors were consumer discretionary (-2.9%), financials (-0.4%), and consumer staples (-0.2%).

Highlight reel: On Monday Meritor (MTOR) +44% to $35.47, Tenneco (TEN) +94% to $19.35 on Tuesday, CarGurus (CARG) +44% to $46.44 on Friday. On the downside, Kodiak Sciences (KOD) -80% to $9.86 on Tuesday, Yandex (YNDX) -40% to $20.32 on Thursday.

Futures action: April WTI crude oil (CLJ2) topped $100/barrel early last Thursday but reversed sharply intraday and ended the week only modestly higher at $91.59. April gold (GCJ2) also spiked after news of the invasion—trading as high as $1,976.50/ounce—but retreated to close Friday at $1,887.60. Biggest up moves: May hard red wheat (KWK2) +7.6%, May wheat (ZWK2) +6.8%, May Brent crude oil (BK2) +4.4%. Biggest down moves: May cocoa (CCK2) -6.1%, May oats (ZOK2) -12.9%, March Russian ruble (R6H2) -11.8%.

Coming this week

Events in Europe may put tonight’s State of the Union speech on more watchlists than usual, while the week concludes with the latest jobs report:

●Today: Advance Wholesale and Retail Inventories, Goods Trade Balance, Chicago PMI

●Tuesday: Markit Manufacturing PMI, ISM Manufacturing Index, Construction Spending, President Biden State of the Union Speech

●Wednesday: ADP Employment Change, Fed Beige Book

●Thursday: Challenger Job Cuts, Productivity and Labor Costs, Markit Services PMI, ISM Non-Manufacturing Index, Factory Orders

●Friday: Employment Report

Retail names dominate the earnings calendar for a second week:

●Today: Lucid Group (LCID), HP (HPQ), Luminar (LAZR), SailPoint Technologies (SAIL), Freshpet (FRPT), GoodRx (GDRX), Workday (WDAY), BigCommerce (BIGC)

●Tuesday: J.M. Smucker (SJM), Target (TGT), Kohl's (KSS), Bayer (BAYRY), AutoZone (AZO), SoFi Technologies (SOFI), Scientific Games (SGMS), Nordstrom (JWN), Salesforce.com (CRM), Ross Stores (ROST), Urban Outfitters (URBN)

●Wednesday: Pure Storage (PSTG), American Eagle Outfitters (AEO), Dollar Tree (DLTR), Abercrombie & Fitch (ANF), Splunk (SPLK), Victoria's Secret (VSCO)

●Thursday: Big Lots (BIG), Kroger (KR), Sibanye-Stillwater (SBSW), Burlington Stores (BURL), BJ's Wholesale Club (BJ), Duolingo (DUOL), Broadcom (AVGO), Gap (GPS), Costco (COST)

●Friday: Hibbett (HIBB)

Check the Active Trader Commentary each morning for an updated list of earnings announcements, IPOs, economic reports, and other market events.

Shocks vs. trends

Apart from the tragic human toll, the global economic repercussions of Russia’s invasion—especially its impact on energy prices, which are pivotal to inflation—are unknown.

Aside from noting the market’s perseverance through multiple wars, natural disasters, and financial crises over the past century, the historical record suggests military conflicts and related geopolitical disruptions are more often shorter-term drivers of volatility rather than longer-term determinants of trend. “Market shock not without precedent” highlighted the tendency for stocks to bounce back after sell-offs like the one that occurred last week, regardless of the source of the disruption.

One implication of this tendency is that the macro factors that were in place before a shock will likely, in time, reassert themselves. As Morgan Stanley Wealth Management strategists noted, the stock market was already facing challenges in an environment of imminent Fed tightening and potentially slowing growth.1 Those pressures will remain after the market fully absorbs the shock of the events in Europe.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.

1 MorganStanley.com. Thoughts on the Market podcast: The Prospect of a Continued Correction. 2/23/22.