A strategy for stalling stocks

- ORCL up more than 25% since mid-March

- Stock paused in recent days after hitting new highs

- Calendar spread can benefit from time decay and falling volatility

Stocks hitting record highs or lows may seem to be of interest mostly to momentum-seeking traders, but they can also attract the attention of those looking to deploy options strategies that can benefit from declining volatility and the passage of time.

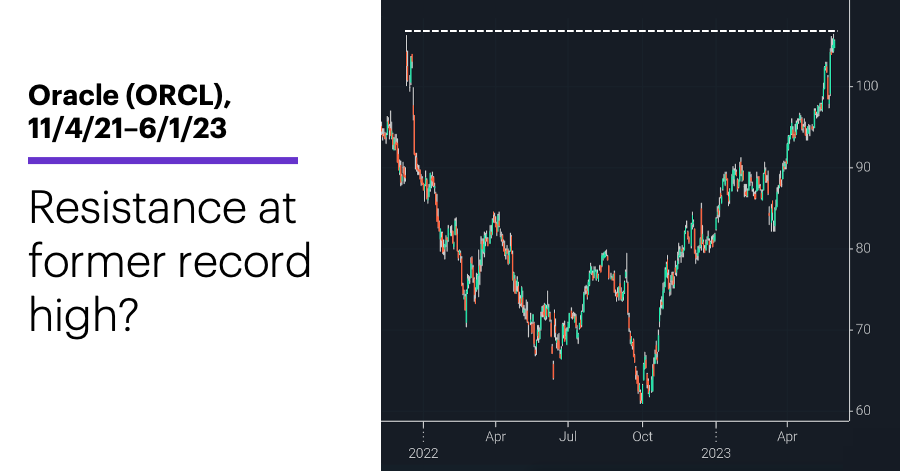

Take a look at Oracle (ORCL), which has consolidated the past few days even as it hit consecutive all-time highs on Tuesday and Wednesday—just a hair above its former record highs from December 2021:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

It’s fair to say that you could find a range of opinions about ORCL’s outlook—just as you could with any other stock. Some traders may think it will break out to fresh highs, while others (noting the stock has rallied more than 70% since September 30 and more than 25% since March 15) may feel it could retreat after testing its former highs.

But what about traders who think the stock may simply…stall? While most stock traders would probably move on to another ticker, options traders can use different strategies to potentially take advantage of markets they don’t expect to do much during a specific time window.

The basic calendar spread pairs a short at-the-money (ATM) option with a long ATM option with a later expiration date. For example, with a stock trading at $50, a trader could short a June $50 call and buy a July $50 option. All options lose value over time, and because they lose it at an accelerated rate as expiration approaches, the June option would be expected to lose more value than the July option.

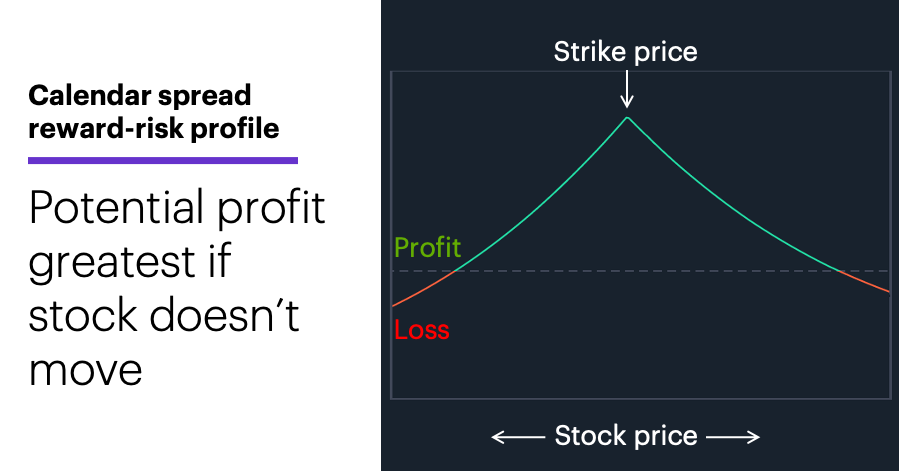

Typically, calendar spread traders exit their positions at or shortly before the nearby option’s expiration, at which point it will have lost all or most of its time value. Meanwhile, the long option will have some time value left—and, hopefully, will have lost less value overall than the short option, thus creating a net profit:

Source: Power E*TRADE. (For illustrative purposes. Not a recommendation.)

As the chart shows, a calendar spread’s potential profit is greatest (at the expiration of the nearby option) if the stock price is unchanged. This is another way of saying the strategy benefits from steady to lower volatility—i.e., losses can occur if the stock moves too far to the upside or downside. In this sense, the calendar spread is a “short volatility” trade—which is precisely why its reward-risk profile is very similar to that of a short straddle.

Today’s numbers include (all times ET): Employment Report (8:30 a.m.).

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights.