Year-end crosscurrents

E*TRADE from Morgan Stanley

12/01/21US stocks ended November not too far removed from their all-time highs, but it may not feel like it to some investors after a rocky final few days provided a sharp reminder of the market’s capacity to surprise—and the importance of staying the course through bouts of volatility.

News of the omicron COVID variant appeared to temporarily shove aside inflation—and virtually every other market concern—to trigger sell-offs in equity and energy markets around the globe, helping turn what had been a positive November for the US stock market into its second down month of the past three.

Last month also highlighted a potential disconnect that could play an important role in the coming months: A stock market that may still be downplaying inflation, despite its increasingly tangible effects on consumers—and a bond market that may be sending a different message about the subject (something our colleagues at Morgan Stanley Wealth Management recently cited as a concern for the stock market1).

Before digging deeper into these crosscurrents, here’s a look at how markets fared last month.

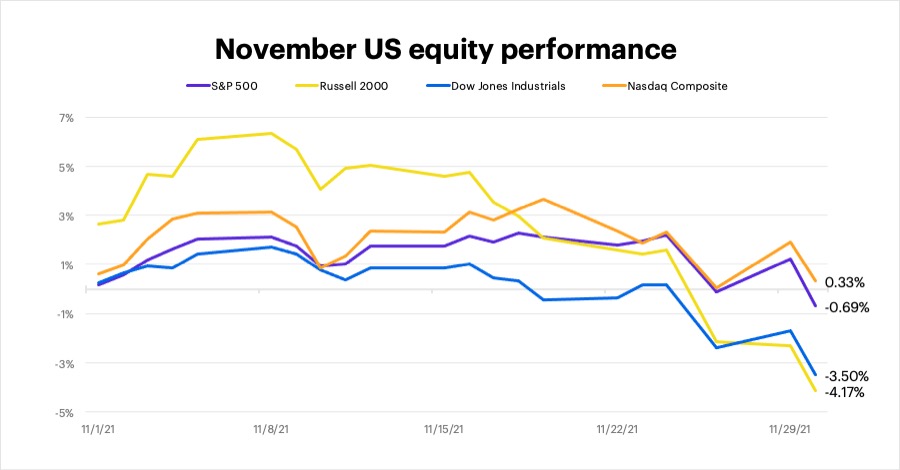

US equities

Although all the major US stock indexes pushed to record highs at some point in November, most of that bullishness occurred early on, and weakness toward the end of the month—punctuated by the COVID omicron sell-off—erased almost all those gains. The tech-heavy Nasdaq Composite was the only US index to end November with a positive return (+0.3%), while the Russell 2000 small-cap index, which led the market early in the month (hitting all-time highs for the first time since March), was its biggest loser (-4.2%):

Source: FactSet Research Systems

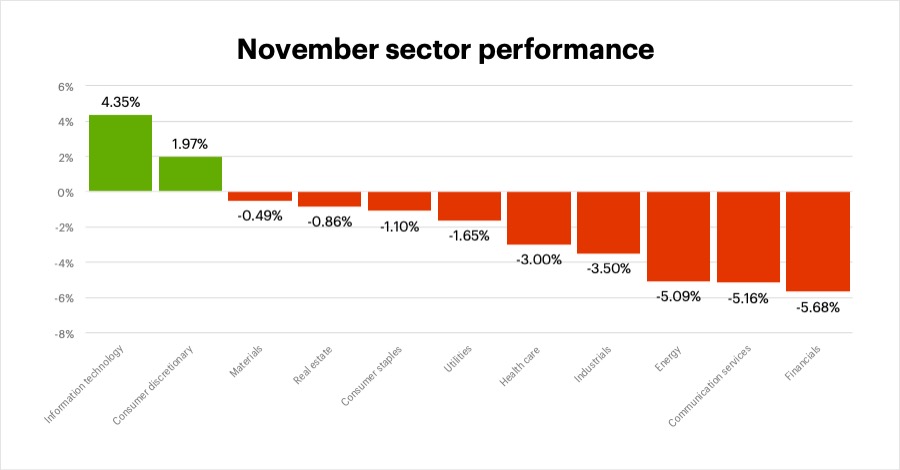

Sectors

Tech was the strongest of the two S&P 500 sectors that managed to post net gains last month. Financials and communication services took the biggest steps back, while energy stocks also retreated sharply as crude oil prices—which had already been drifting lower for much of November—plunged more than 13% in the final three days of the month:

Source: FactSet Research Systems

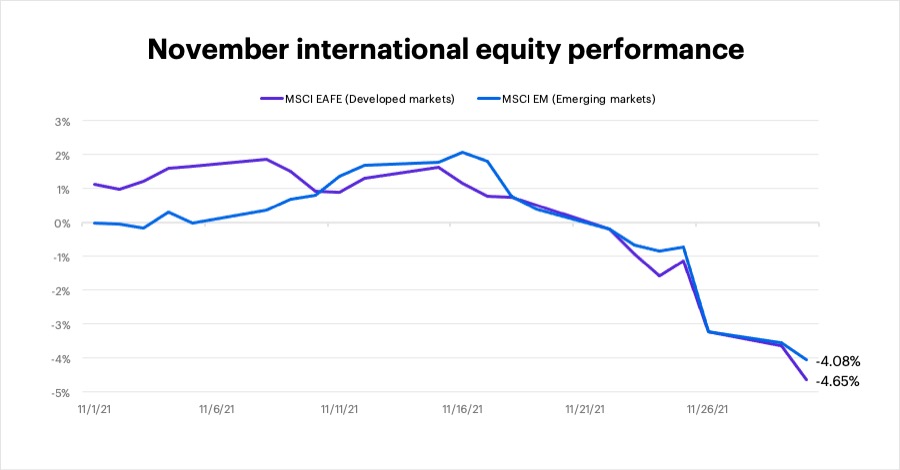

International equities

Overall, international stocks underperformed the US market in November, with developed markets experiencing somewhat larger losses than emerging markets. Possible factors contributing to international underperformance: US dollar strength and weakness in some cyclical sectors that generally have greater representation in broad international indexes than in US indexes. The MSCI EAFE index of developed markets fell 4.7% while the MSCI Emerging Markets (EM) index declined 4.1%:

Source: FactSet Research Systems

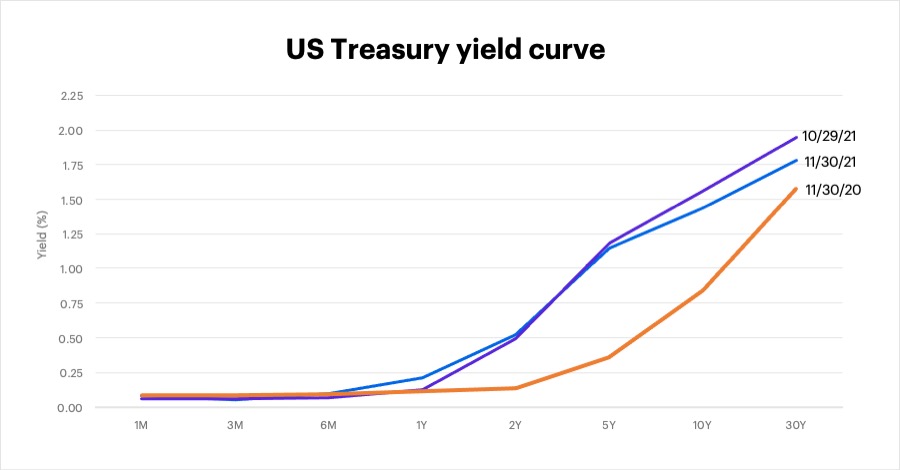

Fixed income

The yield curve further flattened in November as longer-term yields declined for a second-straight month, a possible indication of reduced optimism about long-term economic growth. The benchmark 10-year T-note yield, which climbed to a one-month high of 1.69% on November 24, ended the month at a three-week low of 1.44%.

Source: FactSet Research Systems

Looking ahead

As we head toward the end of the year, here are a few themes that may shape the market landscape:

- Remember September (and late November). The volatility we’ve experienced the past few months may be the template for the foreseeable future. October’s exceptionally strong stock rebound may have erased September’s downturn from the minds of many investors, but the late-November turmoil was a valuable (if unwelcome) reminder that markets that go up without exception are not the norm.

- Inflation: The Fed vs. the bond market. Although minutes from the most recent policy meeting stated the Fed would “not hesitate to take appropriate actions” (i.e., raise interest rates) to address inflation2—and Fed Chair Powell this week mentioned the possibility of speeding up the tapering process—the stock market may not have fully digested this information. The fixed-income market may be looking at things differently, though: Significant increases in intermediate-term (two- to seven-year) yields over the past couple of months suggest bond investors may expect inflation to be higher and/or more persistent than stock investors currently do. If the bond crowd is right, it implies rate hikes may arrive sooner than many people think.

- Interest rates and jobs. The employment picture could play a big role in determining when the Fed may make a move, since it’s cited a stronger labor market as a prerequisite for raising rates. On that score, last month’s employment report was much stronger than anticipated, and jobs growth for both of the previous two months was revised significantly upward. (The next employment report comes out on Friday.) That said, the uncertainty introduced by the omicron variant may influence the Fed’s calculus.

The markets’ ability to surprise—and the volatility that can result—only emphasizes the importance of diversifying among market caps, styles, and even bonds to provide ballast. Although bond returns may still be low, investors shouldn’t dismiss the volatility-dampening characteristics they bring to the table. Maintaining a long-term perspective is all about staying the course, knowing that sometimes the assets that are underperforming in your portfolio today may be the most valuable ones in it tomorrow.

Click here to log on to your account or learn more about E*TRADE's trading platforms, or follow the Company on Twitter, @ETRADE, for useful trading and investing insights

1 MorganStanley.com. Diverging Views on Inflation Could Be a Risk for Investors. 11/23/21.

2 CNBC.com. Fed members ready to raise interest rates if inflation continues to run high, meeting minutes show. 11/24/21.

Head of Portfolio Construction for Morgan Stanley Portfolio Solutions

Mike Loewengart is Head of Portfolio Construction for Morgan Stanley Portfolio Solutions and a Managing Director in the Morgan Stanley Wealth Management Global Investment Office. Mike is responsible for the asset allocation and investment vehicle selections used in E*TRADE from Morgan Stanley’s advisory platforms. Prior to joining E*TRADE in 2007, Mike was the Director of Investment Management for a large multinational asset management company, where he oversaw corporate pension plan assets. Early in his career, Mike was a research analyst focusing on investment manager due diligence for the consulting divisions of several high-profile investment firms. Mike holds series 7, 24, and 66 designations, as well as the Chartered Alternative Investment Analyst (CAIA) designation. He is a graduate of Middlebury College with a degree in economics.

Executive Director, Morgan Stanley WM Global Investment Office

Andrew Cohen is an Executive Director in the Morgan Stanley Wealth Management Global Investment Office. Prior to joining E*TRADE in 2014, he was the Director of Investments and Operations for a large Registered Investment Advisor, where his responsibilities included investment manager research, asset allocation, and portfolio construction. Previously, he was a Senior Research Analyst and Team Leader for Morgan Stanley. He is a CFA® charterholder and a member of the CFA Institute and CFA Society New York. He is a graduate of Virginia Tech with a Bachelor of Science (B.S.) in finance.