Credit 101: Using credit wisely

Morgan Stanley Wealth Management

08/31/21Summary: Whether you’re applying for a mortgage, purchasing car insurance, or signing up with a new internet provider, you will inevitably be asked about your credit. Understanding how this number is calculated and how to establish a healthy credit score early on in life can help increase your financial freedom and purchasing power in the future.

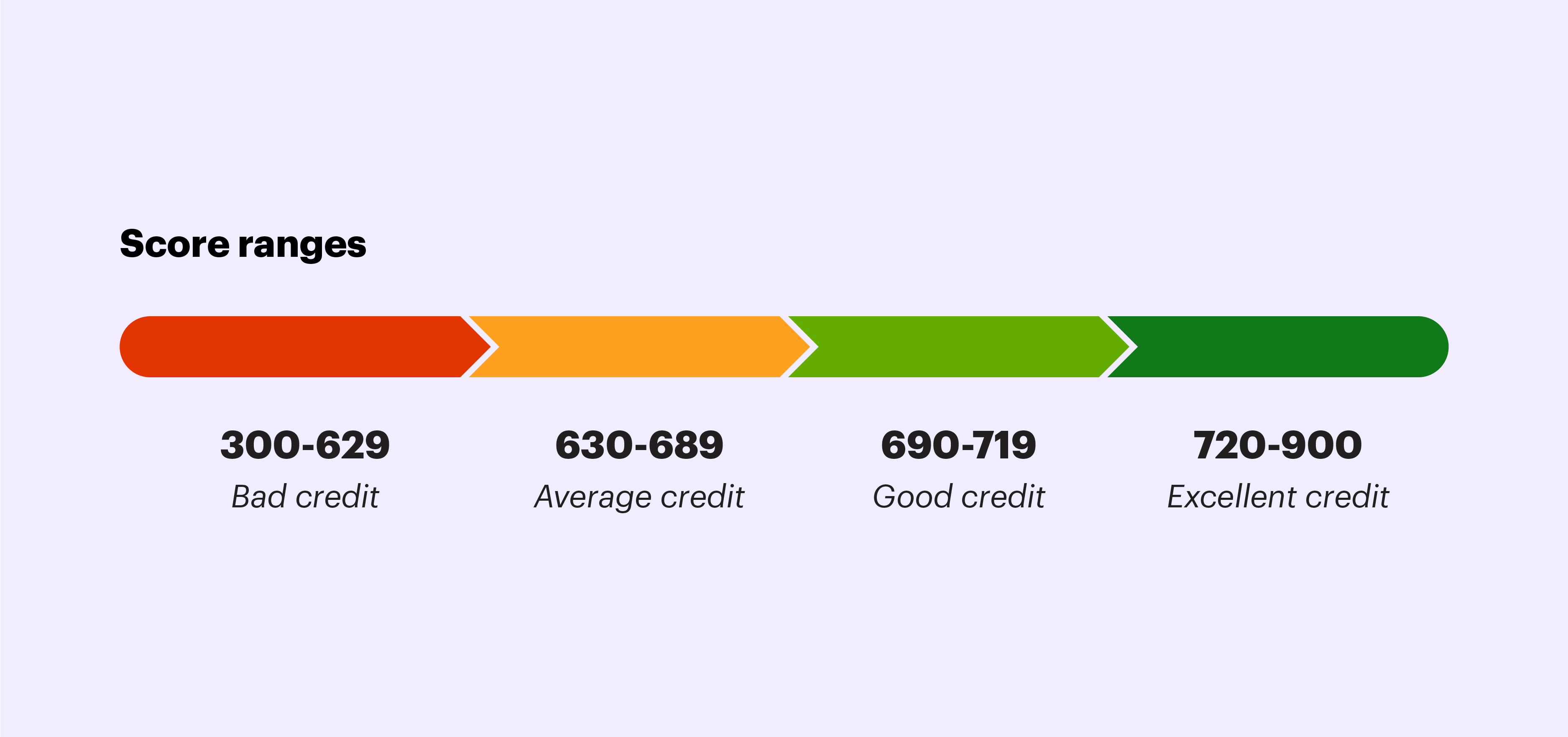

Look at your credit report as your personal financial report card. This report gives you a three-digit score ranging from 300 to 850 that tells lenders how risky you are as a borrower. Every time you pay your credit card balance or repay a loan, the transaction is reported to the credit bureaus and counts toward your total score. A good credit score (690 and above) helps position you as a trustworthy, responsible customer. A low credit score (anything below 630) can have significant implications on your ability to access money and may even result in higher interest rates and down payments because you will be considered a "high-risk" borrower.

You can find out your credit score by requesting a free, online credit report from a national credit bureau (AnnualCreditReport.com is a federally authorized source that offers more information). You are entitled to one free copy a year, or within 60 days of being rejected for credit, employment, insurance, or rental housing due to bad credit.

The magic behind the numbers

The first step to establishing good credit is to understand how your score is calculated. The credit bureaus typically take the following five factors into account:

- Payment history. Paying your bills on time has the greatest impact on your credit score. The credit bureaus prioritize credit card payments over other types of debt like student loans or mortgages.

- Credit utilization ratio. This is the sum of all your outstanding credit balances (your total debt) divided by your total credit limit. In other words, how much of your total available credit are you currently using. For example, if you have a balance of $1,000 on a card with a $5,000 limit, your credit utilization ratio for that card is 20%. Generally, the lower your utilization ratio, the better.

- Length of credit history. The longer your credit history, the better, so try to start building credit as early as possible.

- Total open lines of credit and types of credit used. There are several types of credit that can influence your credit score. In addition to credit cards, your credit score takes car loans, mortgages, student loans, and several other forms of debt into account.

- Number of hard credit inquiries. Checking your own credit once a year may not affect your score, but there are a lot of other people who might be requesting a report on your behalf. Every inquiry made by a third party in your name can have a negative impact on your score, so try and keep these to a minimum.

Winning plays for keeping up your credit

Fortunately, there are several things you can do to maintain or improve your score. Here are some ways to keep your financial report card in good shape:

- Avoid late payments. Late payments on anything from medical and electric bills to credit card dues and monthly rent can cause your credit score to drop and may be noted on your credit report for up to seven years. Credit bureaus typically don’t report late payments until 30 days after the payment is due, but don’t let it get to that.

- Avoid canceling credit cards. Canceling a card will decrease the amount of total credit in your name and lower your credit-utilization ratio as a result, even if you have no balance on a card.

- Avoid applying for several credit cards at once. Credit institutions record all credit inquiries made in your name. Multiple inquiries within a short amount of time can suggest that you might be "high risk", which may have a negative impact on your score.

- Automate payments. Set up automatic payments for your credit cards to avoid being penalized for late payments.

- Make copies. If you know that several people will be inquiring about your credit within a short time period (for example, when moving or applying for a loan), offer to send them a recent copy of your credit report instead of having them each make a formal credit inquiry on your behalf.

- Stay below a 30% credit utilization rate. Keep in mind that your credit score takes your overall credit utilization into account, as well as the credit utilization rate for each individual card.

- Be cautious when co-signing a loan. If your co-signer defaults on a payment, it could have a negative impact on your score too.

- Review your credit report annually. Many credit reports have mistakes that could result in a lower credit score, so make sure to request a report once a year. Not all institutions report to all three credit bureaus, for example.

Whatever your starting point is, don’t underestimate the power of these three digits and remember that it’s never too early to become credit-wise.

The source of this article, Credit 101: Using Credit Wisely (October 2020), is part of Morgan Stanley’s series The Playbook: Your Guide to Life and Money. Learn more about the Playbook and other resources available to help you navigate various life milestones.